Indice degli argomenti

Innovation Contests may be broadly defined “IT-based and time-limited competitions arranged by an organization or individual calling on the general public or a specific target group to make use of their expertise, skills or creativity in order to submit a solution for a particular task previously defined by the organizer who strives for an innovative solution” . Consistently with the purpose of our study, we focus on ICs that involve entrepreneurs as participants and solvers. ICs may be triggered by sponsors (i.e. companies interested in the solutions provided by solvers) and organizers (i.e. actors dealing with all the activities related to designing and managing the initiatives) for a number of different reasons, like finding a pragmatic solution to an existing problem, scouting ideas or startups to acquire, triggering innovation within the sponsor company, or even fostering education and entrepreneurial attitude in the company’s management (following a Corporate Entrepreneurship paradigm). In 2016, our original Research allowed us to map 153 Innovation Contests organized in Italy. An extremely relevant design element affecting the appeal and success of an IC is its reward system. Participants may be awarded through three different alternative systems: Monetary awards or “grants” – amounts of cash provided by the sponsor (or the organizer), to winners of the initiative. They can take three different forms: monetary grants, investments in equity, and loans (debt capital). Non-monetary awards – intangible services and benefits of different nature which aim at assisting the startups’ performances in order to improve entrepreneurial skills of startups’ founders, increase their visibility and support their growth. A combination of both monetary and non-monetary awards.  Our survey reveals that monetary awards or grants coming from ICs are considered by 63% of our sample as a possible complement (rather than a substitute) for Equity financing, followed by Debt financing (35%) and forms of self-financing (2%). Concerning the three alternative reward systems identified, 80 out of 153 Innovation Contests (52% of the entire sample) are characterized by a reward system made exclusively by services, followed by competitions with a hybrid system (49); only 24 Italian competitions only offer a monetary reward. Hence, the typical award is offered in terms of services (whose valuation is extremely complex): this way, organizers and sponsors may refrain from sustaining a real cash outflow, although they are partly neglecting the startups’ need for grant financing. Focusing on much needed monetary awards, the 63 ICs offering grants generate a total 2,773,500 euros; still, 8 competitions also prized the winners with 3,140,000 in Equity investment; and, finally, 5 contests awarded a total 1,773,000 euros through loans. This implies an important message: competitions are extremely important to reach the visibility desired by any startups, but may also represent a good springboard to obtain investments in Equity or get access to loans. Through our Research, we can also evaluate the average monetary grant won by a single winner. The total number of winners of 153 competitions mapped in the sample is 673; while 261 is the number of winners generated only by the 63 contests that offer a monetary grant in the reward system. Hence, considering 2,773,500 euros spread on the 261 winners, a winning team receives 10,626.44 euros on average. This amount is significantly low, and our finding reinforces the claim that grants cannot in any way replace pre-seed and seed investments, but might only act as complementing or enabling financing rounds. Considering non-monetary awards, we grouped the services offered in Italian ICs into six categories: Mentoring (offered in 56 ICs mapped); Incubation Programs (42 ICs); Training Courses (35 ICs); Acceleration Programs (32 ICs); Only visibility and networking (15 ICs); and Other services (e.g. free usage of platforms, internships in well-established companies, discounts, marketing campaigns, legal services, hospitality and accommodations – 42 ICs). Obviously, several ICs offer more than one of these service categories within their award bundle. Our analysis of non-monetary awards reveals how these services are often loosely and inconsistently defined (with specific reference to the notion of “mentoring” and the difference between incubating vs accelerating programs), thus showing the need to consolidate our ecosystem also in terms of foundational definitions. Concerning ICs organizational structure, the most typical one is characterized by the presence of enablers (alone or part of an organizing team) without a sponsor company: this structure is found in 67 ICs out of 153. Alternatively, in 22 cases competitions have at least one enabler in the organizing team and at least one company in the sponsor group; and in 21 cases contests are organized by a Public Authority (alone or part of an organizing team) without a sponsor. It is surprising to notice that although the academic literature on Innovation Contests claims that the best organizing structure would be the one involving an enabler as effective organizer supported by a well-established corporate sponsor, this is not the most recurring organization for Italian ICs currently held: such finding may leave room for a possible redesign of many competitions.

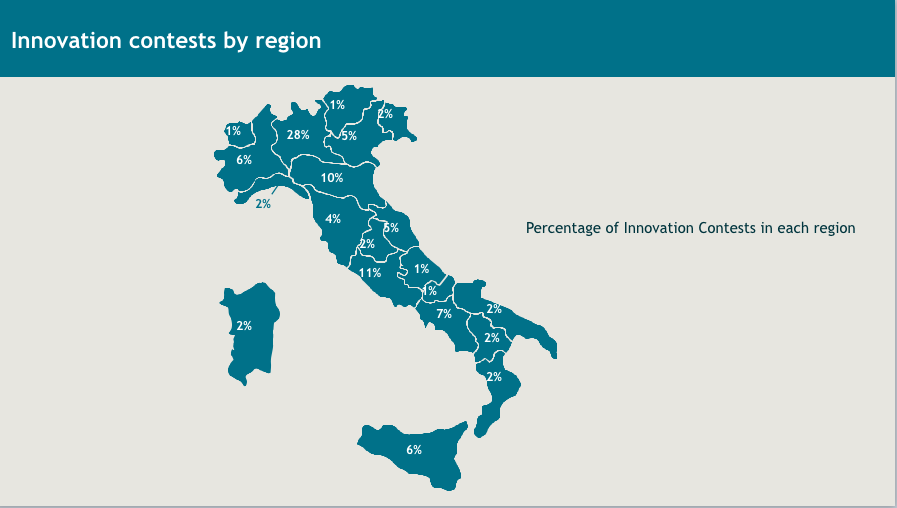

Our survey reveals that monetary awards or grants coming from ICs are considered by 63% of our sample as a possible complement (rather than a substitute) for Equity financing, followed by Debt financing (35%) and forms of self-financing (2%). Concerning the three alternative reward systems identified, 80 out of 153 Innovation Contests (52% of the entire sample) are characterized by a reward system made exclusively by services, followed by competitions with a hybrid system (49); only 24 Italian competitions only offer a monetary reward. Hence, the typical award is offered in terms of services (whose valuation is extremely complex): this way, organizers and sponsors may refrain from sustaining a real cash outflow, although they are partly neglecting the startups’ need for grant financing. Focusing on much needed monetary awards, the 63 ICs offering grants generate a total 2,773,500 euros; still, 8 competitions also prized the winners with 3,140,000 in Equity investment; and, finally, 5 contests awarded a total 1,773,000 euros through loans. This implies an important message: competitions are extremely important to reach the visibility desired by any startups, but may also represent a good springboard to obtain investments in Equity or get access to loans. Through our Research, we can also evaluate the average monetary grant won by a single winner. The total number of winners of 153 competitions mapped in the sample is 673; while 261 is the number of winners generated only by the 63 contests that offer a monetary grant in the reward system. Hence, considering 2,773,500 euros spread on the 261 winners, a winning team receives 10,626.44 euros on average. This amount is significantly low, and our finding reinforces the claim that grants cannot in any way replace pre-seed and seed investments, but might only act as complementing or enabling financing rounds. Considering non-monetary awards, we grouped the services offered in Italian ICs into six categories: Mentoring (offered in 56 ICs mapped); Incubation Programs (42 ICs); Training Courses (35 ICs); Acceleration Programs (32 ICs); Only visibility and networking (15 ICs); and Other services (e.g. free usage of platforms, internships in well-established companies, discounts, marketing campaigns, legal services, hospitality and accommodations – 42 ICs). Obviously, several ICs offer more than one of these service categories within their award bundle. Our analysis of non-monetary awards reveals how these services are often loosely and inconsistently defined (with specific reference to the notion of “mentoring” and the difference between incubating vs accelerating programs), thus showing the need to consolidate our ecosystem also in terms of foundational definitions. Concerning ICs organizational structure, the most typical one is characterized by the presence of enablers (alone or part of an organizing team) without a sponsor company: this structure is found in 67 ICs out of 153. Alternatively, in 22 cases competitions have at least one enabler in the organizing team and at least one company in the sponsor group; and in 21 cases contests are organized by a Public Authority (alone or part of an organizing team) without a sponsor. It is surprising to notice that although the academic literature on Innovation Contests claims that the best organizing structure would be the one involving an enabler as effective organizer supported by a well-established corporate sponsor, this is not the most recurring organization for Italian ICs currently held: such finding may leave room for a possible redesign of many competitions.  One last point about ICs refers to their geographical distribution. The finding stemming from the geographical distribution of Innovation Contests in Italy is in line with that of investments by area: North is confirmed as the hub of the ecosystem as well as of the competitions phenomenon, since 55% of contests are organized in northern Italy. The remaining 45% is almost equally split between South and Islands (23%), and Center (22%).

One last point about ICs refers to their geographical distribution. The finding stemming from the geographical distribution of Innovation Contests in Italy is in line with that of investments by area: North is confirmed as the hub of the ecosystem as well as of the competitions phenomenon, since 55% of contests are organized in northern Italy. The remaining 45% is almost equally split between South and Islands (23%), and Center (22%).

Funded startups versus Innovative startups

The decision to focus the Observatory’s attention on financed hi-tech startups is one of our trademarks, since it comes from the will to consider financings as a tangible measure of startups’ quality and value: this perspective appears particularly interesting when comparing our sample of reference to the broader one of “innovative startups” listed in the special section of the Company Register of the Chamber of Commerce. Registered Innovative startups are significantly increasing, having reached approximately 6745 units as of the end of December 2016. However, an increase in quantity isn’t necessarily matched by a corresponding rise of quality. A comparison of the two samples, in fact, shows that only 70% of startups financed between 2012 and 2015 are also listed in the Company Register. Among the main reasons raised by funded startups for not being in the Register we find: • the sometime limited positive impact perceived by the management team that doesn’t consider the listing essential, believing they can rely on the founders’ professional background and for being required to bear an opportunity cost in terms of time to manage the registration process; • a sort of “cultural distance” between startups and some Chambers of Commerce, leading the first to not fully agree with the eligibility logic of the Register, while the latter have some problems in understanding or certifying the innovative requirements of applying startups. This cultural difference can result in twisted behavior, with startups that, if rejected by a Chamber of Commerce, may transfer their company headquarters to a different jurisdiction and thus gain a new registration opportunity; • the existence of excellence centers supporting startups (such as Universities, Research Centers, R&D units of large enterprises or districts) offering a protection framework that can be viewed as an alternative to registering. Also to further strengthen its role in speeding up the ecosystem’s growth, in 2015 the Italian Government changed its approach towards public financing of innovative startups: from granting non repayable monetary awards (such as those provided by Invitalia Smart&Start), that appeared to be a simple and inexpensive financing source for startups but did not necessarily require involvement and professional support, to shifting to investments management through formal investor Invitalia Ventures that, in line with Venture Capital funds role, guarantees a combination of Equity capital and management support.

Adoption of Public Instruments

Within this year’s Research we also submitted a survey on our population of Italian funded hi-tech startups aimed at analyzing the adoption of Public Instruments launched by the Italian Government to support innovative startups. A first finding from our survey shows how 70% of funded startups are listed in the Innovative Startups Register, while 30% of them are not: this finding is consistent with the percentages showed by our total population. This fact demonstrates how our stratified sample reached by the survey resembles the overall population (which shows the same result). Focusing on the 35 non innovative startups, only 4% of them were founded in 2016, while 21% were founded in 2015, 12% in 2014, 21% in 2013 and 42% in 2012. This underscores how the decision not to be listed in the Register is not influenced by the startup’s youth (that is, younger startups did not have the time to register), but on the contrary, 96% of the unregistered startups are older than 2 years. While 32% are listed in the Innovative SMEs Register (thus showing a good continuity and integration between the Innovative Startups and Innovative SMEs Registers, which is actively promoted by MISE – the Italian Ministry for Innovation and Economic Development), when we delve more deeply into the motivations behind the decision of not being listed, the following reasons emerge: 18% of the sample declared the Register offered limited contribution to the startup’s perceived standing, which was already guaranteed by the entrepreneurial team’s background; 18% answered that they expected limited contribution to the startup’s likelihood to raise additional funding; 9% see an opportunity cost related to managing bureaucracy; 9% of the startups are not listed since they changed their business name; 5% of them argue that the Register offers limited contribution to the startup’s degree of innovativeness (already guaranteed by incubator/accelerator/certificated body); and the remaining 9% is equally split between startups declaring a lack of time (4.5%) or misalignment with the Register’s intended purpose and startup’s internal policies (4.5%). Our survey also investigated which funded hi-tech startups listed as innovative actually took advantage of the Public Instruments made available to them. What is striking is that 40% of our sample (made of 82 startups) declare they never used any facilitation whatsoever, showing how getting access to such facilitations is not a top priority for them. Considering the remaining 60% of startups which took advantage of the Public Instruments offered, the alternatives most frequently accessed to were: “Fondo di Garanzia” (24%); “Credito d’imposta R&D” (22%); and “Disciplina dei contratti a tempo determinato” (16%).  Within this subsample of those startups who benefited from Public Instruments, 24 out of 49 of them took advantage of just 1 instrument; 14 startups contemporarily got access to 2 instruments ; while 5 startups used 3; 4 startups used 4; and 2 startups used 5. No startup in the sample used more than 5 instruments at the same time. Among those instruments startups feel the Italian Government should enhance or introduce, we list: fiscal pressure relief (38%); incentives to sponsor companies investing in startups (28%), which again confirms the interest from hi-tech startups in collaborating with well-established companies; higher incentives in R&D investments (25%); industry regulation favoring startups (6%); and regulatory measures for fair competition (3%).

Within this subsample of those startups who benefited from Public Instruments, 24 out of 49 of them took advantage of just 1 instrument; 14 startups contemporarily got access to 2 instruments ; while 5 startups used 3; 4 startups used 4; and 2 startups used 5. No startup in the sample used more than 5 instruments at the same time. Among those instruments startups feel the Italian Government should enhance or introduce, we list: fiscal pressure relief (38%); incentives to sponsor companies investing in startups (28%), which again confirms the interest from hi-tech startups in collaborating with well-established companies; higher incentives in R&D investments (25%); industry regulation favoring startups (6%); and regulatory measures for fair competition (3%).

Hi-tech startups and strategy: Business Model Design & Innovation and strategic objectives

Our survey on Italian funded hi-tech startups also considers significant strategic dynamics occurring in our ecosystem. More specifically, we focused on investigating: if and how Italian funded hi-tech startups changed and innovated their business models (BMs); and which strategic objectives they set in the short vs mid-long term. A business model is a company’s architecture of value: it describes how companies create value for their target customers, as well as how they capture a share of such value to be profitable and sustainable. By studying startups’ business model innovation dynamics, we can disclose insightful elements related to their adoption of strategy and innovation-related models and approaches like the Lean Startup. Two thirds (66%) of the hi-tech startups analyzed declared they changed their business model since they were founded: this information proves how Steve Blank’s definition of a startup as a “temporary organization designed to search for a repeatable and scalable business model” is correct, since changing how value is created and captured is an inherent trait for the large majority of the sample. The depth and magnitude of the change introduced also varies: while 59% of the sample declared they incrementally changed their business model, 41% stated that such innovations were even radical. By considering the “Business Model Canvas” as a construct to visually represent the startup’s architecture of value, we could also underscore where such changes took place and which business model’s parameters and building blocks were impacted. Incremental change most frequently affected the startups’ parameter of value proposition (21%), followed by customer relationship (17%), customer segments (14%), key activities (13%), channels (12%), key partners (9%), key resources (6%), cost structure (4%) and revenue streams (4%). This proves that the changes preached by the Lean Startup approach do not necessarily focus on the value proposition (i.e. the bundle of products and services the startup offers to its target customers), but they also penetrate other dimensions. If these single parameters are grouped together in the three BMs’ building blocks of Value Proposition and Interface, Value Infrastructure and Value Formula, our Research shows that 64% of the changes affect Value Proposition and Interface, while 28% impact the internal Value Infrastructure and 8% modify the Value Formula. This finding testifies how addressing actual customers’ pains and gains and solving a relevant job with the right offer is often a crucial task for a startup; as a consequence the need for a proper alignment between external interface with customer and internal activities, resources and competencies endowment emerges, in order to guarantee the right execution; the business model’s viability in terms of its revenue streams and cost structure appears to be subject to less frequent testing. Concerning the breadth of change, i.e. the number of BM parameters changed within the same startup, those startups declaring they underwent an incremental change modified from 1 to 7 parameters, with a peak in the range 2 to 4 parameters. In 89% of cases, more than 1 parameter was changed, showing how BM innovation dynamics propagate within the same BM to ensure internal consistency. When the change was radical, 96% of the startups interviewed showed they changed more than 1 parameter, with a peak corresponding to a change in 4 parameters (32%); all the 9 parameters were altered in 8% of the cases, whereas a radical change is more likely to propagate throughout the BM. Moving to the second objective of our strategic investigation of Italian funded hi-tech startups, we analyzed what objectives startups declare they set in the short vs mid-long run. Startups give the highest priority on the following short-term objectives: turnover growth (28%); further acquisition of Equity financing (16%); total number of users growth (14%); and internationalization (14%). This shows how Italian startups look for cash flow or Equity as a top priority in the short term, probably because of the relative shortage of significant pre-seed and seed investment rounds in the ecosystem; these startups do aim for growth and traction thanks to an increased number of user (that is specifically true for Digital startups), while they are seldom “born global” (i.e. seeking an international expansion upfront). Other relevant objectives they refer to are business model consolidation (consistently with our previous analysis on BM change), enhancement of the entrepreneurial team with more varied and professional skills, and collaboration with well-established companies or incumbents. As the time horizon expands, hi-tech startups declare turnover growth is still the number-one priority (25%), while internationalization gains second place (20%); further acquisition of Equity financing (12%) and users growth (12%) are again at the top of the list. The fact that these main strategic goals do not change significantly as we move from short to mid-long term shows how Italian startups perceive their evolution takes time, and it is apparently not easy to strategically shift to the next stages of their lifecycle; exponential, disruptive growth is in fact not that common in our ecosystem, due to its structural limitations. Hi-tech startups also declare they will need to further enhance their team in the mid-long term. The necessity to consolidate their business model decreases over time as they move from a temporary to a scalable organization. When we further compare short with mid-long term objectives, it is interesting to notice how exit through trade sale is sought for in the long run by 7% of startups: this further proves our finding, according to which a more systematic and structured strategic interaction between incumbents and startups (which possibly ends up with an acquisition) could constitute an important evolutionary path for the Italian ecosystem; and startups are aware of this. IPO, instead, is not seen as a real option (only 1% of the sample shows a long-term interest in it). Concerning debt financing, only 2% of the sample states they would be interested in collecting it in the long run: this result testifies how startups often see debt as a way to acquire capital only consolidated companies should rely on, and may explain why a number of funded hi-tech startups do not resort to the Public Instruments offered to facilitate debt acquisition.

Methodology

The findings presented in the report are the result of four main research activities performed by the Hi-tech Startups Observatory of the School of Management del Politecnico di Milano (in collaboration with Italy Startup): • quantifying investments in hi-tech startups made by formal and informal players in Italy; • evaluating main performances and dynamics of financed startups; • surveying the Italian funded hi-tech startups ecosystem to map the role of Innovation Contests, analyze the Italian Public instruments’ impact, and investigate startups’ strategic dynamics in terms of business model change and strategic objectives set; • the analysis of a selection of significant Italian startups in terms of financing rounds, revenue and exit. 1 – Investments in hi-tech startups in Italy The quantification of investments in risk capital or “Equity” of Italian hi-tech startups was done within the following boundaries: • startups with registered offices in Italy operating in the “hi-tech” sector – divided into the macro sectors “Digital”, “Life Sciences”, “Cleantech & Energy” and “Other”; • investments from formal players– independent Venture Capital funds (IVC), Corporate Venture Capital funds (CVC), Regional Financial companies – and informal players – Venture Incubators, Family Offices, Angel Networks (or Club Deals), Business Angels and companies without structured CVC funds – with offices in Italy. The quantification was performed through primary sources. Several direct interviews have been conducted, involving: • all formal investors, with the addition of main informal players; • all startups financed in the September 2015 – October 2016 timeframe by the players mentioned. Additionally, primary sources have been integrated with secondary sources, in order to guarantee data triangulation. The investments from international players in 2016 figures, as well as the calculations considered to quantify the international formal investments inflow vs outflow, are estimates that take into account large operations communicated through secondary sources or emerged from primary sources: these estimates can therefore be subject to adjustment in future updates. In order to provide a more comprehensive view of informal investments, we collaborated with the Crowdfunding Observatory of the School of Management del Politecnico, and IBAN (Italian Business Angel Network). The Crowdfunding Observatory (in the person of Prof. Giancarlo Giudici) supported our estimate of invested amounts with successfully closed Equity Crowdfunding campaigns, while the collaboration with IBAN (in the person of Prof. Vincenzo Capizzi) supported us in evaluating the Angel Investing component that contributes to the informal investments part (an extract of IBAN 2015 survey results has been added to our collection of data from primary sources. For additional information please go to: www.iban.it). Benchmarking on domestic investments in startups made by formal European players was performed through a comparison of our data with information published by the secondary source Invest Europe (http://www.investeurope.eu/), integrated with data from the leading European VC associations: • EVCA – The European Private Equity and Venture Capital Association (http://www.investeurope.eu); • BVK – Bundesverband Deutscher Kapitalbeteiligungsgesellschaften (http://www.bvkap.de); • AFIC – Association Française Des Investisseurs Pour La Croissance (http://www.afic.asso.fr); • ASCRI – Asociación Espanola De Entidades De Capital (http://www.ascri.org). The data used was collected throughout October 7, 2016; included due to their significance, are 2 financing rounds occurred the 14 November 2016 (TAG) and 15 November 2016 (Musement). 2- Performances and dynamics of financed hi-tech startups Data collection leveraged a combination of primary and secondary sources. The primary source was a survey on startups financed in the 2015-2016 timeframe.The secondary sources used for the integration of primary sous were: • Aida, the database populated by the Bureau van Dijk Edizioni Elettroniche Spa (http://www.bvdinfo.com/it-it/home); • Official Italian Chamber of Commerce data archives (www.registroimprese.it). The combination of primary and secondary sources enabled to achieve data triangulation and solve potential divergences of information from secondary sources. As regards 2015, any missing data was rebuilt through a consistent combination of assumptions presented in the 2015 Report of the Hi-tech Startups Observatory (see for more details). More specifically, as concerns 2015, excluding startups ceased in 2012, 2013 and 2014 and those founded in 2016, it was necessary to rebuild revenue data for 48 startups (10.4%) and information about hired employees for 22 startups (4.8%). The data regarding the “innovative startups” sample refers to the contents of the Special Section of the Company Register: http://startups.registroimprese.it. The data used was collected throughout October 7, 2016. 3- Italian Public instruments’ impact on startups dynamics and startups business models On early 2017 the Hi-tech Startups Observatory launched a survey on the overall population of Italian funded hi-tech startups . The total respondents to this survey are 117 startups: such stratified sample shows alignment ad consistency with the overall population’s characteristics, which ensures its significance and representativeness. The survey’s goals and samples were the following: • to map the adoption and role of Innovation Contests in 2016. This section of the survey was supplemented by an extensive research based on both primary and secondary sources, which led to the identification of 153 Innovation Contests organized in Italy; • to analyze the adoption and perception of Public Instruments offered by the Italian Government to support the startup’s ecosystem. The respondents to this section of the Survey is equal to the overall sample (117 respondents), made by 82 innovative startups (70%) and 35 non innovative startups (30%); • to investigate the strategic dynamics of the startup’s ecosystem, in particular with regard to the startup’s business model change and the strategic objectives set. The respondents to this section of the Survey is equal to 61 startups. 4- A selection of significant startups This section presents cases of Italian hi-tech startups characterized by significant performances in the three main phases of their lifecycle: • “introduction” (intended as entry in the financed startups sample) measured through financing received in the last available year; • “growth”, measured in terms of revenue generated in Italy in the last available year; • “consolidation” or “exit”, measured in terms of exit value for “trade sale” (or acquisition by other companies) or “Initial Public Offering” (IPO) in the last available year. A regards these three lifecycle phases of hi-tech startups, the case selection criteria adopted were: • startups with the highest financing rounds over the last year; • startups with the highest revenues registered in Italy in 2015; • startups with a significant exit value over the last year. The analysis of startups with the highest financing rounds in 2016 and the highest revenues in 2015 considered only startups with the following characteristics: • registered offices in Italy; • financed by formal and informal national and international investors (no branches in Italy). The analyses of startups with a significant exit value over the course of the last year considered only startups with the following characteristics: • italian main investor; and/or; • italian founder; and/or; • registered offices in Italy; and/or; • R&D headquarters in Italy; and • exit value either declared or disclosed Where possible, the data was collected from primary sources. The missing data was obtained through secondary sources. The data used was collected throughout November 15, 2016 – Antonio Ghezzi – Professor – Politecnico di Milano Professor of Strategy & Startups & Research Director Hi-tech Startups Observatory

© RIPRODUZIONE RISERVATA