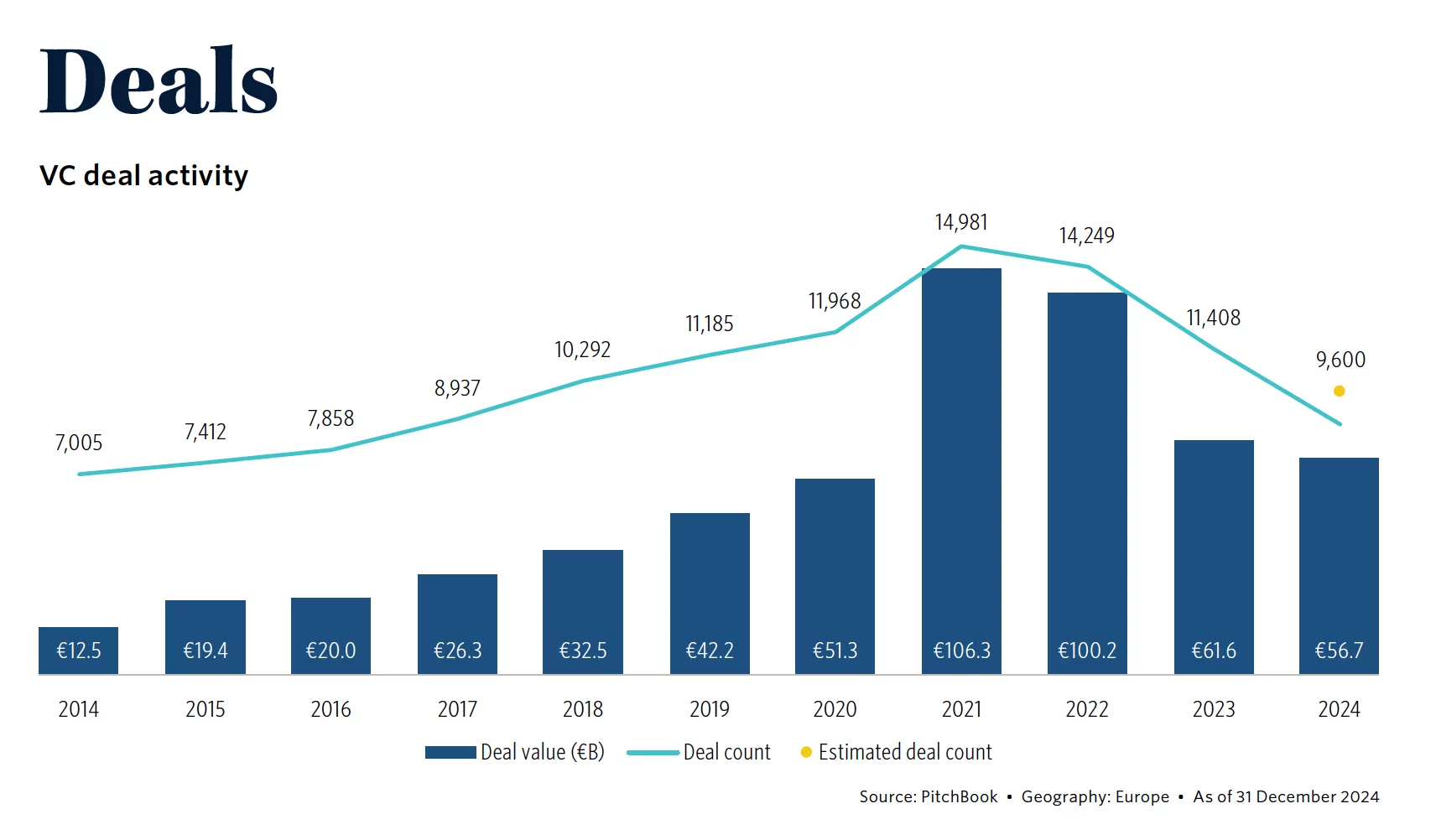

The value of venture capital (VC) deals in 2024 in Europe has slowed down. The figure is negative despite the macroeconomic recovery and the growth of venture capital. The decline shows an overall figure of EUR 56.7 billion in value compared to EUR 61.6 billion in 2023, which was already a decline from over EUR 100 billion in 2022 and EUR 106 billion in 2021. This is the main finding of the Pitchbook report on the performance of venture capital activities in Europe over the past year.

Valuations improved, but the decline in the number of deals was more pronounced as the focus on quality and the emphasis on the profitability of companies increased. The number of transactions increased from over 11,000 in 2023 to about 9600 in 2024. Despite the inflection of deal activity, capital availability remained limited and the time between rounds continued to lengthen. Interest rate clarity supported the recovery in valuations, but growth prospects remained mixed, contributing to a tone of cautious optimism throughout the year. As expected, artificial intelligence (AI) was one of the prevailing sectors, however, investment growth in life sciences almost matched the rate of increase in AI.

The annual value of venture debt transactions increased significantly during the year from EUR 13.5 billion in 2023 to EUR 17.2 billion in 2024, supported by megadeals from venture-growth operators.

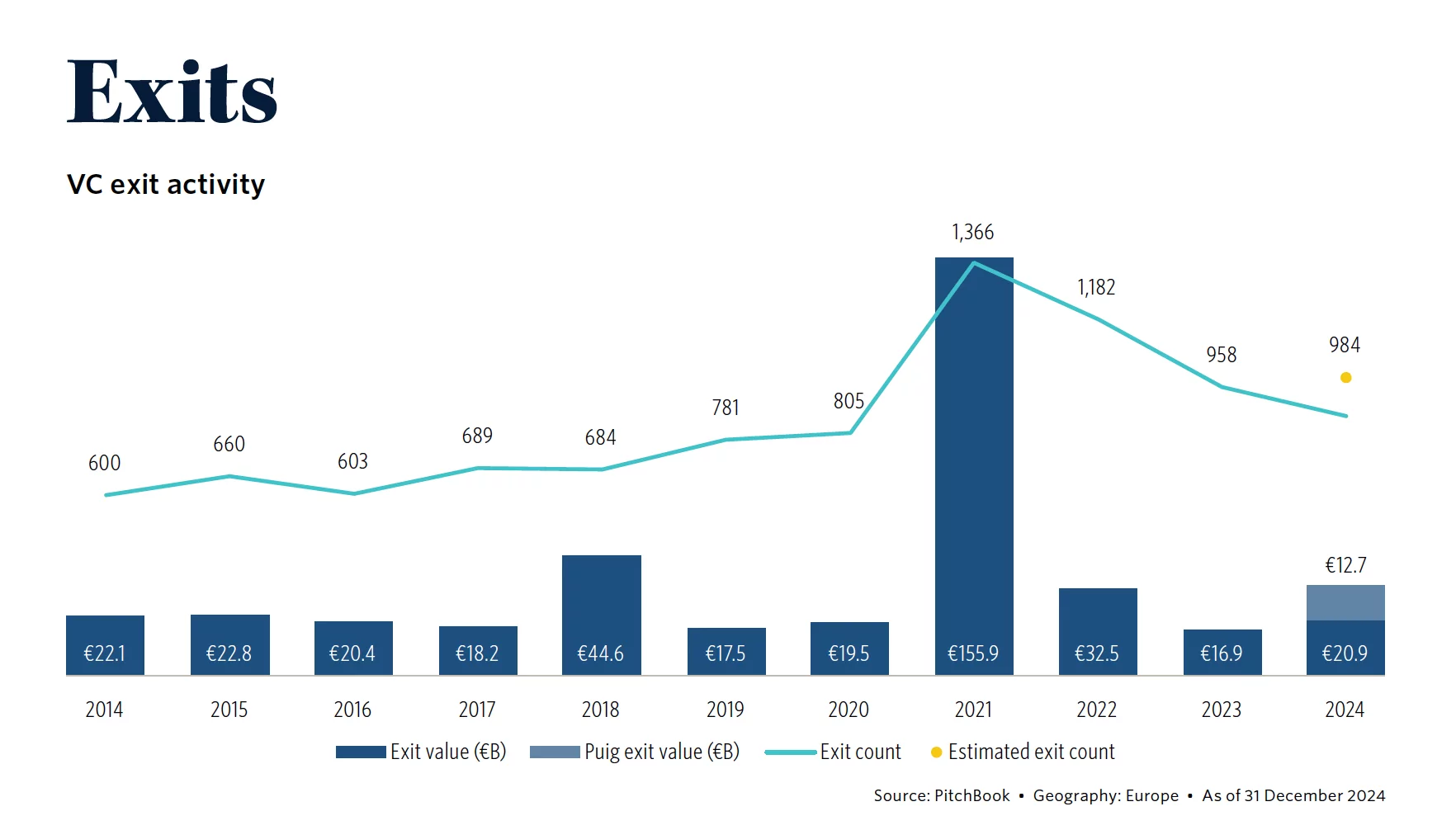

2024 was the year of the return of exits. Despite a quiet fourth quarter, the annual value of exits increased by almost 24% year-on-year, even excluding the large Puig listing, which alone weighed EUR 12.7 billion of the EUR 33.6 billion total. The upswing was concentrated in several large transactions, with the life sciences and artificial intelligence sectors driving the value of exits.

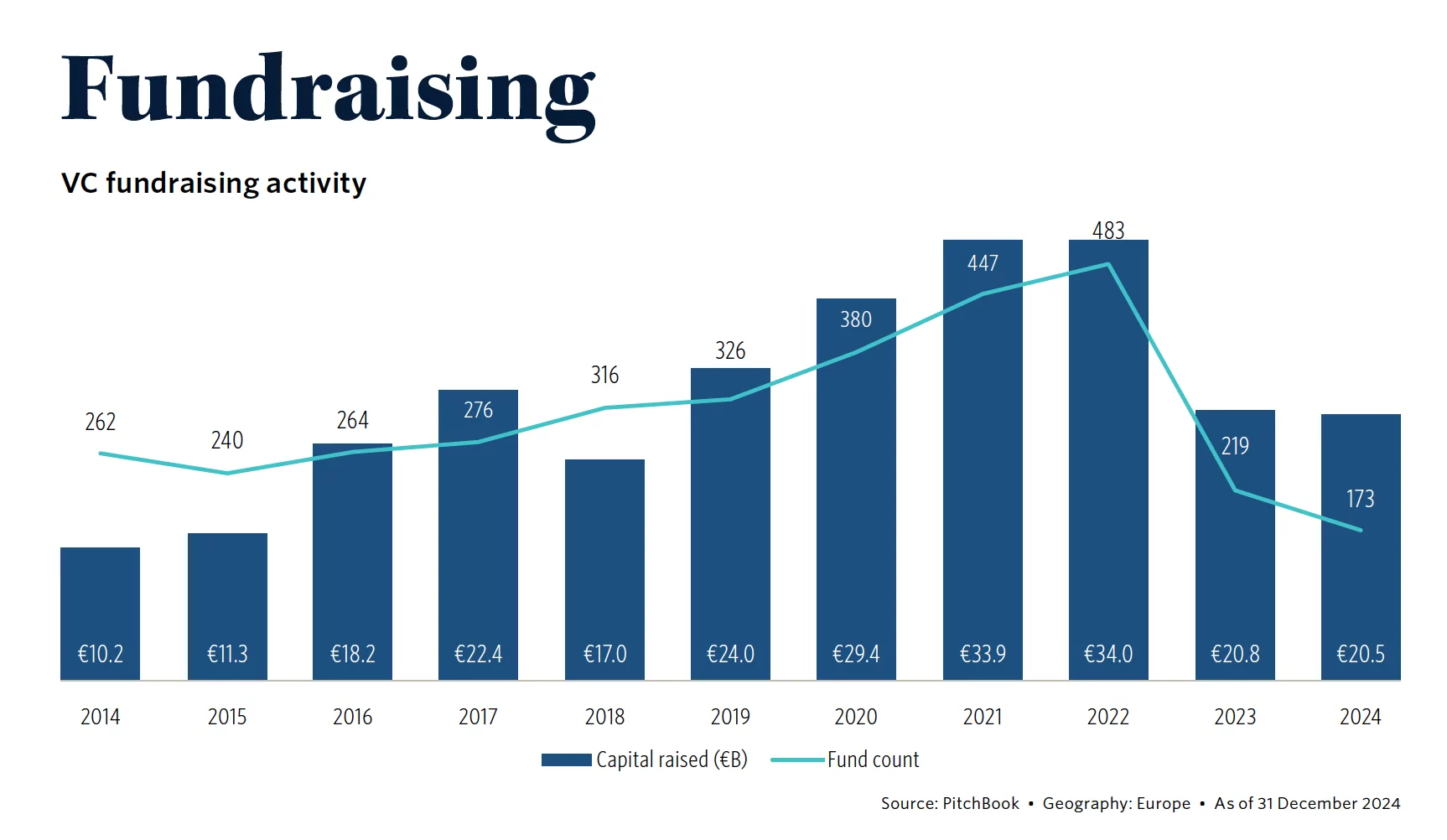

Fundraising remained essentially stable compared to the previous year, EUR 20.8 billion in 2023, EUR 20.5 billion in 2024. The size of funds has increased and there are 173 active funds compared to 219 last year. Many of these vehicles are located in the UK, increasing the region’s share of capital raised in Europe, however, Southern Europe also increased its share with significant closings, especially in Spain. Despite the longer closing times, new vehicles also increased their share of funds.

ALL RIGHTS RESERVED ©