Design Economy 2024 is the new edition of the report that highlights how the design industry is important for the country’s economy, not only in terms of industry, production, exports, job creation, but also in terms of culture, training, technology adoption, innovation and active support for sustainability and inclusion issues.

The report was produced by the Symbola Foundation together with Deloitte Private, POLI.design, ADI and in collaboration with Comieco, AlmaLaurea, CUID, under the patronage of the Ministry of Foreign Affairs and International Cooperation and the Ministry of Enterprise and Made in Italy.

The aim is to raise awareness of the value of design for the competitiveness of the national production system and the presentation of the report at the ADI Design Museum in Milan was attended by Ermete Realacci, president of the Symbola Foundation; Ernesto Lanzillo, Deloitte private leader in Italy; Luciano Galimberti, president of ADI; Cabirio Caution, CEO POLI.design; Domenico Sturabotti, director of the Symbola Foundation; Antonio Grillo, design director Tangity Design Studio – NTT Data; Maria Porro, president of the Salone del Mobile; Marco Maria Pedrazzo, designer manager; Susanna Sancassani, managing director METID – Politecnico di Milano; Francesco Zurlo, Dean of the School of Design Politecnico di Milano; Lorenzo Bono, Head of Research and Development at Comieco; Adolfo Urso, Minister of Enterprise and made in Italy.

“Italian leadership in design confirms its important role as an intangible infrastructure of Made in Italy and a protagonist in the challenge of sustainability. In the midst of a green and digital transition – declares Ermete Realacci, president of the Symbola Foundation in a note – design is once again called upon to give shape, meaning and beauty to the future. Many aspects of our lives, as well as many sectors, are changing: from the metamorphosis of mobility towards shared, interconnected and electric models, to the processes of decarbonisation and the circular economy that are changing industry and supply chain relationships. Products, in a context of scarce resources, will necessarily have to be redesigned to become more durable, repairable, reusable. The relationship between design and sustainability is the basis of the new European Bauhaus launched by President Von der Leyen to contribute to the realization of the European Green Deal and also for this reason Italy is a natural protagonist. Because, as written in the Assisi Manifesto, courageously facing the climate crisis is not only necessary but represents a great opportunity to make our economy and our society more human-friendly and therefore more capable of the future.”

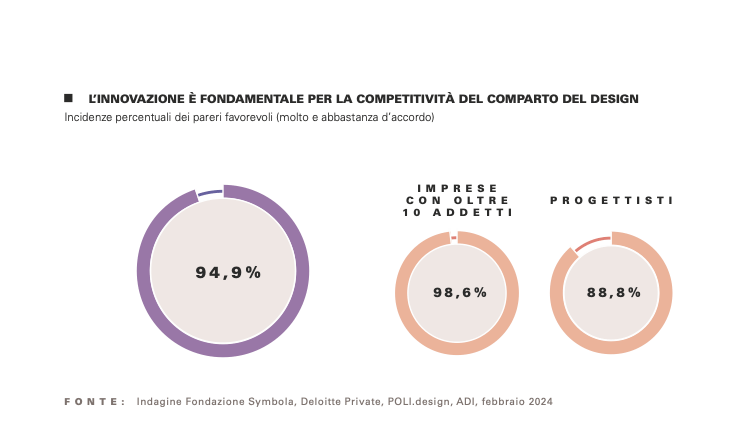

“Italy is the beating heart of European design, boasting records among the 27 EU countries in terms of employees and turnover in the sector. To distinguish our country, in addition to the dimensional primacy, there is also the level of innovation of design made in Italy, which is now considered a fundamental element for competitiveness – comments Ernesto Lanzillo, partner and leader of Deloitte Private in Italy -. To maintain the competitive advantage held so far, Made in Italy Design companies and designers will also have to invest in artificial intelligence, a technology with extraordinary potential that is already being tested by the most cutting-edge companies in the sector and for which the skills of designers will become increasingly important to maintain a human-centered approach”.

“For years we have been accustomed to interpreting the role – says Cabirio Cautela, CEO Poli.design – and the activity of a designer in a manufacturing key. In a profoundly changing scenario, we are observing the emergence of designers who operate as creators of digital content, designers who manipulate organizational aspects once the prerogative only of human resources or designers related to new fields such as biology – the bio-designer – or law, such as the legal designer. As POLI.design we always look for a balance between training opportunities linked to traditional industries and initiatives that anticipate the training of tomorrow’s professionals, ready today to enter competitive contexts that work on the frontier of innovation and experimentation”.

“Timely knowledge and qualitative reading of the data on Italian design,” adds Luciano Galimberti, president of ADI, “on its economic consistency, on the companies that practice it and on the training of its professionals are a fundamental prerequisite for any reliable interpretation of the phenomena that characterize it year after year. For this reason, ADI, which is a direct observatory of Italian design, participates with commitment in the work of qualitative evaluation from which Design Economy was born, an effective tool to achieve the central objective of the association: the dissemination of the culture of design in the world of production and social life”.

The economics of design in Italy and Europe

The sector has 41,908 thousand operators in the design sector, divided between 24,596 freelancers and self-employed workers and 17,312 companies, which have generated an added value of 3.14 billion with 63,485 thousand employees. The companies are distributed throughout the national territory, with a particular concentration in the areas of specialization of Made in Italy and in the regions of Lombardy, Veneto, Emilia Romagna and Piedmont, where 60% of the companies are located. It is in terms of business turnover that Italy is at its best, recording the best performance among EU countries, ahead of the excellent results also achieved by France, Spain and Poland. In fact, in just one year, between 2021 and 2022, sales in the sector grew by +27.1%, which is almost double the EU average (+14.4%).

The capital of Italian design is Milan: the Lombard capital is able to concentrate 18% of the added value of the sector on the national territory. Milan is also home to the Salone del Mobile and the Fuorisalone, the world’s largest event dedicated to design. This trend goes hand in hand with the general one, given that companies and design professionals carry out their activities mainly in metropolitan centers, where they have the opportunity to enjoy greater national and international visibility.

The regional distribution of the data reveals the strong concentration of design activities in Lombardy and specifically in the province of Milan. In fact, Lombardy accounts for 29.4% of Italian companies, 32.7% of added value and 27.7% of total employment. Three other northern regions are confirmed to follow: Veneto (second in terms of share of companies 11.4%, third in terms of value added, 11.4% and third in terms of employment, 11.7%), Emilia Romagna (third in terms of share of companies, 10.5%, but second in terms of added value, 13.5% and employment, 13.3%) and Piedmont (fourth in terms of share of companies, 8.3%, fourth in terms of added value, 10.9% and fourth in terms of employment, 11.0%).

If Lombardy is in the lead among the regions, Milan is in the lead among the provinces and confirms the position noted in previous reports: the area concentrates 14.4% of companies, 18.8% of the added value produced and 13.3% of national employment.

In second place in the ranking for the number of companies is the province of Rome (6.6%), third for product (5.4%) and employment (5.9%), followed by Turin (5.0% but second for value added, 7.2% and employment, 7.1%), Florence (fourth for share of companies, 3.1%, fifth for added value, 2.9% and seventh for employment, 2.6%), Bologna (fifth for share of companies, 2.8%, fourth in terms of value added, 3.7% and employment, 3.6%).

Design and green transition

The issue of environmental sustainability emerges as relevant for the sector: the level of expertise spread shows medium-high values for almost all the operators interviewed (88.0%, an increase compared to 86.9% in the previous report), with a peak of 96.4% for companies with more than 10 employees. Confirming the importance of the topic, as many as 74.8% of those interviewed underline its importance in ongoing projects.

Considering all the companies and designers interviewed, about a third are currently engaged in activities related to packaging design, a value that reaches 50% if we consider designers alone. Looking at the reference materials, paper or materials predominantly made of paper (53.2% of cases) is now the main choice, and remains so also for the realizations of the near future, even if with a decreasing trend. This is followed by the design of packaging using plastic or predominantly plastic materials (12.8%). Also with reference to transitional materials (temporary installations, signage, etc.), paper and materials predominantly made of paper are most used (23.4%).

Among the growing uses, bio-based materials (a family of materials or products mainly polymeric that derive from plant biomass) stand out, with a share of use more than doubled in the forecasts of use in the next three years, from 9.2% to 19.9%. When choosing paper and cardboard as sustainable design materials, the importance of certifying them as coming from sustainably managed forests (FSC, PEFC, etc.) is underlined in particular by design professionals, underlined by almost half of the interviewees (47.0%).

Emerging Design Professions

New to this edition is the in-depth analysis aimed at identifying emerging figures related to design in Italy. The study led to the identification of 20 new emerging professional figures that highlight how the field of design is intertwined with innovation, organization and technologies, confirming the changing and interdisciplinary nature of the designer.

Italy follows a global trend that sees designers moving into areas other than the traditional ones of design, demonstrating that the skills of the design world are versatile and applicable to a wide range of new emerging sectors. At the same time, the traditional figures of design – related to industrial design, architecture, furniture, fashion – are also undergoing transformation, hybridizing traditional skills related to the project with those of marketing, organization and business strategy, and advanced technologies.

Among the emerging figures in design, those with whom the designer segment is most familiar, we find transdisciplinary professions such as the material designer, the designer for accessibility and inclusion and the design engineer. On the other hand, companies are more familiar with more vertical and specific figures such as digital content strategists and information designers. Both designers and companies agree on the relevance of the emerging figure of the prompt designer/designer for AI, able to create a bridge between technology and the practical needs of customers.

Training

In the 2022/2023 academic year, 95 institutes activated courses of study in design disciplines, 3 more than in the previous survey. Among these there are 30 Universities (of which 20 public and 10 private), 26 Other Institutes authorized to issue AFAM titles, 20 Academies of Fine Arts, 13 Legally Recognized Academies and 6 ISIAs, for a total of 344 courses of study, distributed in various educational levels and in different areas of specialization. Compared to the previous year, the number of accredited and activated courses grew by 5% and the number of institutes by 3%, particularly in the case of Universities and Academies of Fine Arts and Legally Recognized Institutions. It is not only the number of institutions and courses that are active, but also the demand and the number of students, equal to 16,423, which is 8.6% more than in the previous academic year.

This growth is moderated by the limited number of admissions to almost all types of institutions. For example, for university degree courses, most of which are subject to the constraint of the programmed number, the number of enrolments in the entrance test is increasing, which exceeds the available places by four times, with a national average of 2.5 applications for each place and peaks of over 6 in northern Italy. Constant relationship over the years despite the growth of active courses of study. The analysis of the geographical distribution of institutes and students enrolled in the first year offers a snapshot of the places where design education takes place. In general, it is widely spread throughout Italy with different levels of concentration. Although in absolute numbers this is higher in the North (40% of institutions and 56% of students), the growth dynamic of new enrolled students particularly rewards the Centre (+25.6% in the last two years and +16.5% in the last year) and the South and the Islands (+13.6% compared to last year).

Digital and artificial intelligence

Among the technologies considered most relevant by the sector is extended reality (40.6%) which, with its immersive tools, enables new forms of collaboration, encouraging creativity, improving training and opening up new business opportunities. This is followed by predictive and generative artificial intelligence (37.7%), for its ability to support and make design activity more efficient, automating some phases, generating ideas and concepts, simulations and advanced prototypes.

If today the level of technological competence of designers appears high, overall 83% of those interviewed in the report consider it medium or high, the preparation on AI-based technologies is still limited overall, in line with the national context: only 45% evaluate their level of knowledge as medium-high. The limited understanding of how AI works and the opportunities arising from the introduction of AI currently translates into a reduced use in design: only just over 3 out of 10 respondents make regular use of it. Among the obstacles to the spread of generative AI we have language barriers, software tends to provide more accurate results when queried in the programming language, and age, the average age of designers is often inversely proportional to computer skills.

The advantages of using AI are optimization of project development time (42.0%), greater customization of products, better services and user experience (37.7%). A value linked to the complementarity and synergy between the two intelligences: human and artificial.

The report can be freely downloaded from the Symbola Foundation website

ALL RIGHTS RESERVED ©