The second quarter of 2024 marks a 48% decrease in terms of the amount invested in startups compared to the first quarter of the year. A value that appears dramatic and as such must be considered but which must also be considered in a broader picture that still sees a semester that does not shine, according to data collected by Growth Capital and Italian Tech Alliance, but which is still in line with the trend of European trends and still sees investor confidence for the second half of the year quite solid.

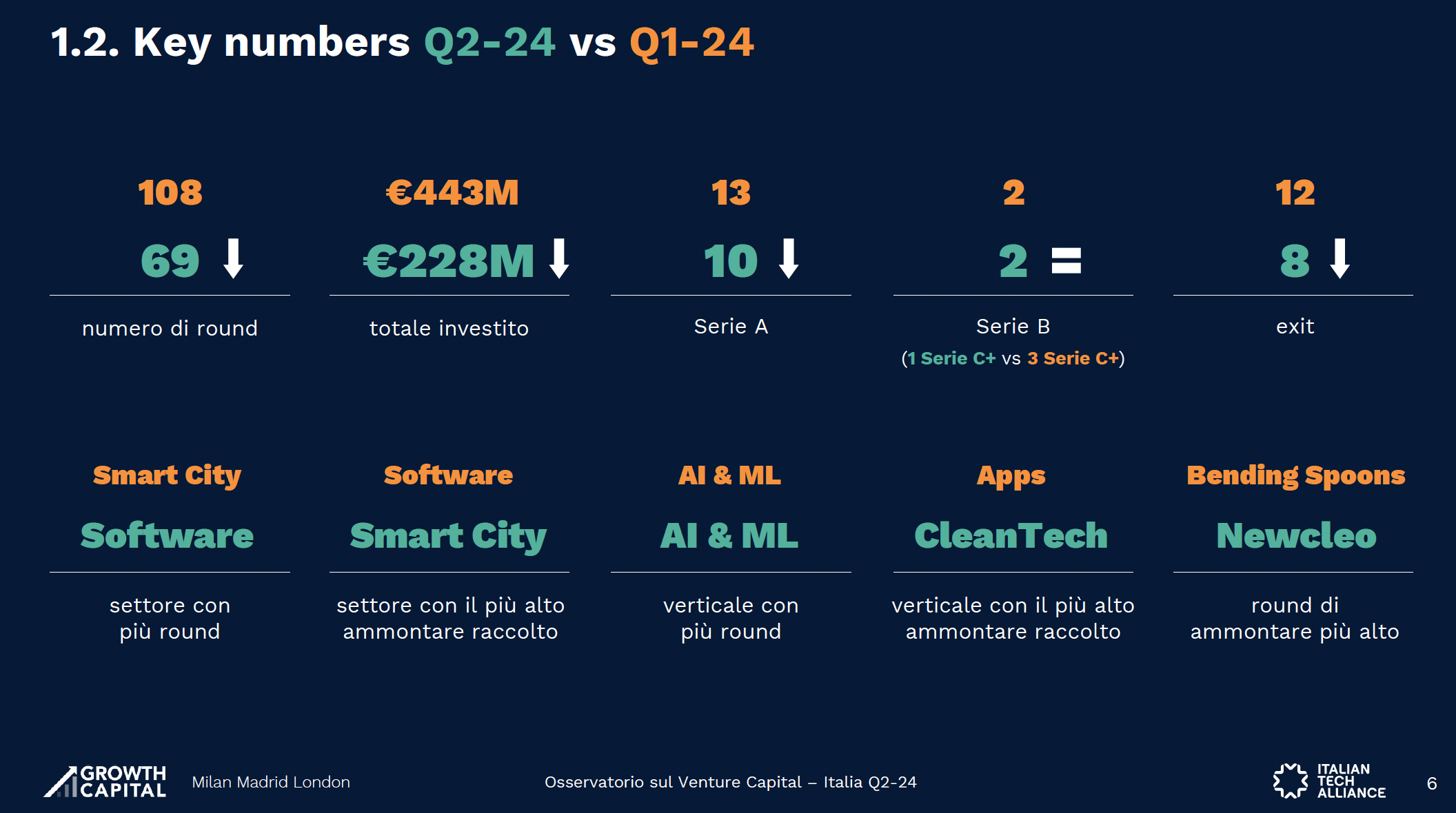

In the second quarter of 2024, €228 million was invested in 69 rounds (of which 10 Series A and 2 Series B, 1 Series C). The sector with the most rounds was software, while smart cities were the one that recorded the highest collection. The most important round in terms of amount raised was that of Newcleo, which closed at 87 million euros. Eight exits in the quarter.

The event presenting the data for the second quarter and the first half of the year saw the participation of Francesco Cerruti (Italian Tech Alliance), Fabio Mondini de Focatiis (Growth Capital), Zaccaria Orlando (McKinsey) Clelia Tosi (Fintech District) and in the round table Giovanni Calabrese (Sella), Giuseppe Donvito (P101/Italian Tech Alliance), Aurora Maggio (Zefi.ai) and Mattia Montepara (Sibill). Mondini de Focatiis illustrated the data by pointing out that European VC shows signs of recovery, with 28 billion euros raised in 5,640 rounds, in the first half of 2024 (recording +18% the number of rounds and +3% the amount invested compared to the second half of 2023). The second quarter recorded €15 billion in funding in 2,320 rounds (+25% of the amount invested compared to the first quarter), despite the number of rounds being 30% lower than in Q1.

In Italy, €671 million was raised in 177 rounds in the first half of 2024, with 37% of the invested amount coming from 2 mega rounds. However, the first half of 2024 is in line with the second half of 2023, but with an uneven distribution between quarters. While looking at the second quarter, the €228 million raised in 69 rounds marks a significant drop compared to the previous quarter, with €87 million attributable to the Newcleo round alone. Again, if we look at the numbers for the half-year, the first of 2024 is still stable compared to the second of 2023.

Looking at the segmentation of rounds by type, in the second quarter of 2024 71% is represented by pre-seeds or seeds. There are only two Serie B for an amount of 21 million, which explains the slowdown in the overall results of the quarter.

In the second quarter of 2014, software was the sector that recorded the highest number of rounds (13), thanks to the growth peak recorded in the AI sector. This is followed by life sciences with 11 rounds and deeptech with 7. Looking at the entire first half of 2024, in line with the 2023 trend, software, life sciences and smart cities are the sectors with the highest number of rounds. Smart cities, on the other hand, are the sector that attracted the most capital in Q1 (95 million), followed by life sciences (37 million) and fintech (33 million). Analyzing the top 5 deals of Q2-2024, we find Newcleo (87 million, Serie A) in the lead, followed by Banca Aidexa (16 million, Serie B) and Futura (14 million, Serie A). Fourth position for Tes Pharma (10 million, Series A) and fifth for Beta Glue Technologies and Avaneidi , which closed an 8 million round, respectively Series C and Series A.

The VC Index, an indicator on a scale of 1 to 10 calculated every six months and which provides an indication of the stage of development of the VC ecosystem in Italy and the sentiment of its players, has fallen compared to the previous six months, signaling a stable environment that tends towards underperformance. All quantitative indicators remained stable or worsened (and in particular exit activity) and at the same time the lack of optimism recorded by operators six months ago is confirmed.

“In a delicate market environment, characterized by high interest rates, inflation and difficulty in making successful exits, we are witnessing greater difficulty in closing capital raisers and increasingly complex deals in the structure. Trader sentiment remains stable compared to six months ago and the market is expected to recover in the coming quarters, which will depend on a variety of factors. Among these, CDP’s role will be of crucial importance: the 3.5 billion euros in investments planned over the next 4 years and the ratification of the new business plan will be able to give new impetus to the Italian ecosystem, creating a positive knock-on effect on direct and indirect investments,” comments Fabio Mondini de Focatiis, founding partner of Growth Capital, in a note.

“The second quarter of 2024 was expected to be a decisive period for a qualitative leap in the Italian innovation ecosystem. The presentation of CDP Venture Capital’s new business plan on the one hand and the imminent launch of the Startup Act 2.0 on the other foreshadowed a new centrality of VC, potentially accompanied by a continuation of the growth in investments seen in previous months – says Francesco Cerruti, general manager of Italian Tech Alliance – . Instead, the downward numerical picture is accompanied by a framework in which, despite the announcements, the Government has not yet presented the Startup Act 2.0, which we are convinced can represent a fundamental tool to strengthen an ecosystem that has already shown that it can contribute to the economic and social well-being of the country”.

An acceleration towards the approval of new regulations and the injection of new capital is more than urgent, especially in a scenario that sees Italy catching up some ground compared to the other major European economies which, however, are not standing idly by, as evidenced by the launch of the new startup fund of the EIB (European Investment Bank) in favor of innovative companies born in Spain, a fund whose first tranche is for €350 million and is wanted by the president of the EIB in office since December 2023 who is precisely the Spanish Nadia Calviño.

The slowdown shown by Italian fintech in 2023 continued in the first half of 2024: in fact, it went from 510 million euros raised in 2022 in 39 rounds, to 142 in 2023 in 29 rounds and down to 41 million in the first half of 2024 in 15 rounds. In the second quarter of 2024, the fintech in Italy raised a total of €33 million in 6 rounds. Despite marginal improvements in the amount invested compared to the first quarter, there have been no major rounds since 2022, which has led to a slowdown in the sector. In Italy, fintech accounts for about 10% of rounds (in line with the industry average), while in the past it catalyzed about 30% of investments, with a significant contraction in the last 18 months. The decline in the average size of rounds coincides with a lower participation of international investors, usually involved in large rounds.

“The fintech world is now at a crossroads: on the one hand, the potential to transform the financial sector is still great and the prospects for fintech revenue growth are very good (+18% per year in Europe until 2028); on the other hand, only some players will be able to stand out in a less favorable funding environment than in the past. Looking ahead, it will be essential for fintechs to focus on profitability, controlling costs, and pursue more balanced and sustainable growth in the long term,” says Zaccaria Orlando, associate partner at McKinsey.

In this scenario, within the Fintech District community, the largest at national level with 295 Italian or foreign fintechs and techfins active in Italy, the value of the investments raised is about 15 million euros, of which about 60% raised in the second quarter. The total is the result of 4 transactions, which took place in the areas of wealthtech (Axyon.AI), business & personal finance management (Sibill), crypto & defi (CheckSig), and techfin/AI (Indigo.AI). From the perspective and spirit of open innovation, corporate venture capital (CVC) represents an important tool because it allows large companies to give further innovative impetus, combining business objectives with investment objectives,” says Clelia Tosi, head of Fintech District.

“Open innovation, by leveraging the creativity and drive of start-ups in the development of new services and technological solutions, serves to stimulate both internal innovation and that of customers and individuals with whom we synergise through our ecosystem. It is an articulated formula to implement but it is the most powerful for innovating and promoting an open financial ecosystem, also having a positive impact on the economy and society,” underlines Giacomo Sella, head of the corporate & investment banking division of the Sella group.

ALL RIGHTS RESERVED ©