Table of contents

The evolution of private equity: an IPO 2024

In a changing world and market, private equity is also adapting to new technologies. Private equity strategies and tools are changing. Over the past decade, PE has increasingly adhered to the needs and timelines of investors and investees. The effects of the

contraction

recorded in 2023 also led to further changes in the EP: Secondary market private equity has been aSignificant acceleration: In 2023, the transaction volume reached $108 billion, up 20% from 2022 In This article provides an overview of Rivate Equity strategies.

Period 2015-2019

Until 2019, private equity funds used

buy-and-build

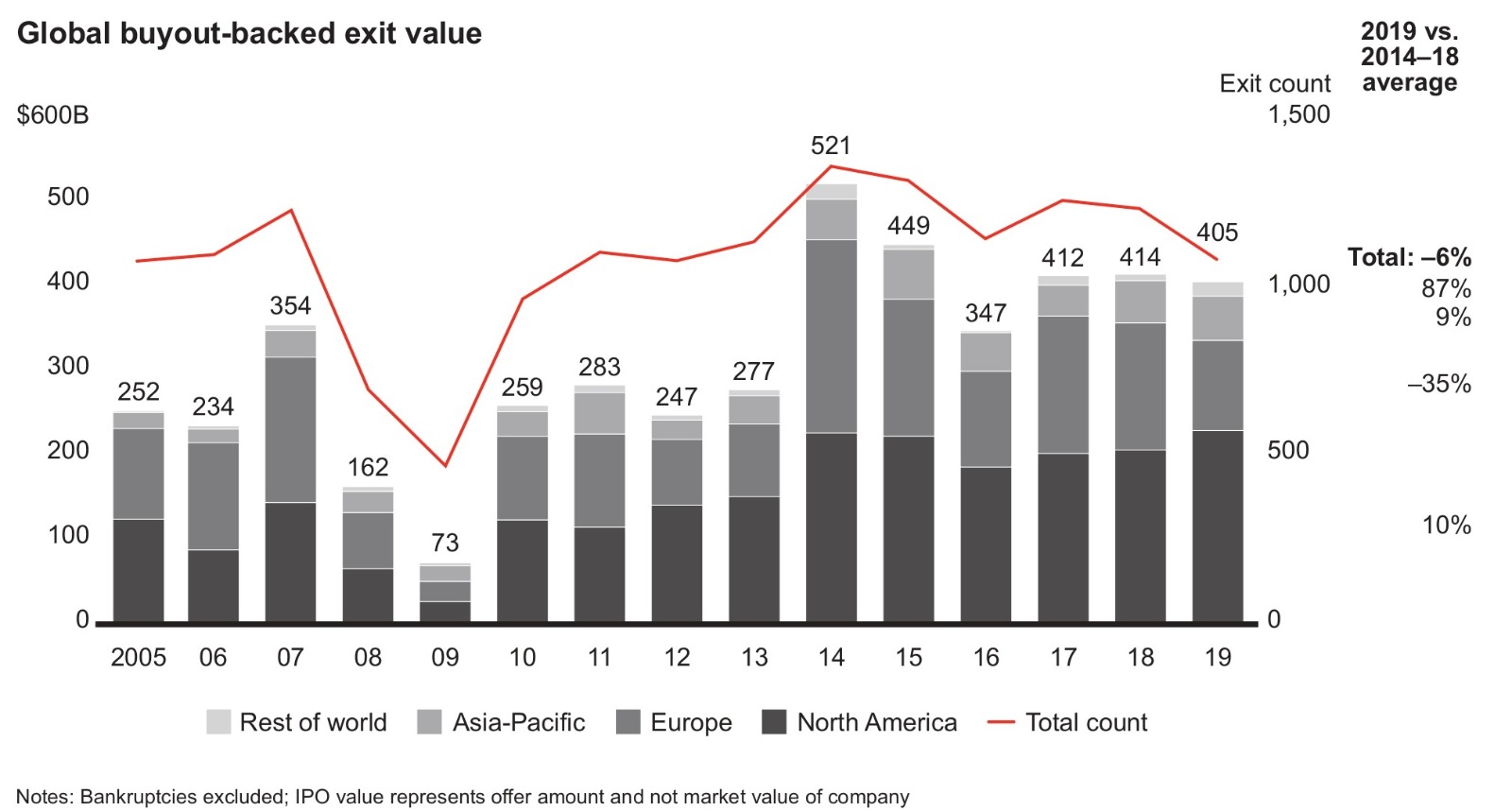

strategies, which allow them to generate much more value and increase revenues, through the acquisition of more small companies. By combining their operations, the funds were able to increase the value they created, thanks to synergies and economies of scale. The numbers for 2018 and 2019 confirm this: investments for a total of 559 billion euros, imposing itself on the scenario of alternative investments, led by hedge funds, but with the aim of bringing as many companies as possible to listing on the stock exchange. And the net cash flow trend of private equity investments has remained positive since 2013. In this context, buy-outs represent the main item of PE transactions and 2018 was the record year in Europe, with transactions exceeding €374 billion. While GPs had a fixed time limit – no more than 10 years of life – between 2015 and 2019 they adopted shorter logics: divestments tended to be carried out over shorter time frames, as shown in the figure below:

Bain & Company: Global Private Equity Report 2020

The growth in PE has been significant: Global capital raised rose from $1.2 trillion in 2015 to $1.9 trillion in 2019. Several factors have contributed, including strong global economic growth, low interest rates , and increased demand for alternative investments. EP’s strategies have included investing in sustainably operating companies, acquiring fast-growing technology and media companies (e.g., Alibaba, Spotify, and Lyft), healthcare , and infrastructure (e.g., water management, energy, and telecommunications companies). An increase in the size of transactions – in 2019, the average of transactions exceeded $100 million – and an increased focus on cross-border transactions – in 2019, about a third of transactions were cross-border. Finally, an increase in the use of structured finance instruments, such as convertible bonds and mezzanine loans, to finance their acquisitions.

Period 2020-2023

Despite the covid-19 pandemic, private equity has continued its growth. Capital raised increased from $1.9 trillion in 2020 to $2.9 trillion in 2023, thanks to factors such as:

- The strong global economic recovery has increased demand for products and services, creating investment opportunities.

- The low volatility of the financial markets has made PE a more attractive investment option for investors.

- The growing focus on ESG investing has led to an increase in demand for investments in companies that operate sustainably.

Private equity strategies during this period have always been focused on the technology and media sectors (with acquisitions of fast-growing companies such as TikTok, Discord and Netflix), infrastructure and healthcare (with the acquisition of companies such as Moderna, BioNTech and Elevance Health). While initially, at the dawn of the pandemic, the immediate focus of GPs was to give stability to companies already in their portfolios,

over time they understood the importance of researching and selecting new investment opportunities

, to gain an advantage from lower asset valuations in certain sectors. In addition, private equity funds have begun to focus on more diversified investment strategies, investing in companies of different sizes, in different sectorsand in different geographies. Then from 2019 onwards, PE investments increasingly tend to make

permanent capital

transactions: examples in 2022 were those of General Atlantic, which launched a new $10 billion permanent capital fund or Microsoft’s acquisition of Activision Blizzard for $68.7 billion, financed in part by a $5 billion permanent capital fund from Berkshire Hathaway. There have also been interesting implications in M&A : in 2021, the ceiling of one trillion in investments was recorded. The increase in the private equity market between 2020 and 2023 continued to take place in the size of transactions – in 2023, the average number of transactions exceeded $200 million -, an increase in cross-border transactions – in 2023, they were about half of the total -, and a continuous increase in the use of structured finance instruments. These strategies have helped to make the global private equity market more competitive and diversified. However, the private equity market began to slow down in 2023, due to a number of factors, including rising inflation and interest rates, which would have made PE a less attractive investment option for investors. And the resulting economic uncertainty would have resulted in a reduction in demand for alternative investments. It explains how

co-sponsor deals

have been one of the most adopted strategies in private equity: in 2023, about 30% of PE deals were co-sponsor deals.

Private equity, hedge funds and SPACs

An example of the evolution of private equity is certainly the one involving hedge funds. They have much higher assets at their disposal and invest not only in companies or private companies but also in listed companies and in a very speculative way. Private equity, even if closed-minded, can invest directly in a hedge fund or co-invest with them in a target company. And the tech sector has always been cannibalized by hedge funds. Unfortunately, their operations haven’t grown lately. Just a year ago, the Goldman Sachs Hedge Industry VIP ETF (GVIP), worth $151 million, plunged 23%. And this week’s news sees E. Shaw’s largest hedge fund return just under 10% in 2023. The $60 billion firm reportedly gained 9.6% in its flagship Composite fund (Bloomberg). The hedge fund market in 2023 has slowed down compared to previous years. Total hedge fund assets fell by 10% in 2023, to $3.6 trillion. This is the first annual decline in hedge fund activity since 2008. Private equity can make the same investments and co-investments in SPACs, companies that go public, sell shares to the public, and then use the proceeds to merge with other companies or acquire them. But the various companies that acquired the status of listed company during the SPAC boom in the pandemic period, reported criticalities in their reporting and internal control processes, and, after two years of bubble, their decline in 2022 and 2023 continues to persist: in 2023, 499 SPACs were listed on the stock exchange, raising a total of $152 billion. This is a 60% drop from 2022, when 1,208 SPACs were listed raising $629 billion.

In Europe

In Europe, even though there were fewer private equity deals than in 2022 or 2021, the 2023 total is still higher than in all previous years. According to data from PitchBook, as of December 13, 2023, €613.8 billion (about $672.8 billion) has been traded in more than 5,724 deals: “zooming in on 2023 acquisitions, there were 4,663 with a total value of €555.2 billion. This is a decrease of 17.3% compared to the total value of the transaction for the whole of last year of €671.3 billion.”

The evolution of the EP

More and more PE companies would have the prospect of going public in 2024. Despite the blow to GPs in the first 10 months of 2023 – deals down 8.3% and deal value down 25.3% compared to 2022, mirroring the rest of the private markets, GP transaction volume saw an increase in the first weeks of the fourth quarter, and industry players remain optimistic about continued market growth in 2024: “managers hoping to sell a stake and buyers looking to deploy capital,” said Mustafa Siddiqui, head of Blackstone’s GP holdings business. On the other hand, private capital fundraising is taking longer than it has done in the last ten years: the average period between the opening and closing of a private capital fund has reached 15.8 months, the highest value since 2012. Between the setback of large buyouts and the drastic decline in EV/ebitda valuation multiples in 2023, a new wave of IPOs would remain among the best solutions/effects for PE companies in 2024

. In times of crisis, relying on it would seem to be the most convincing choice: the public offering route can be attractive at a time when liquidity is limited. How not to forget that some of the largest companies went public in the wake of the global financial crisis (e.g. Blackstone in 2007). Last December, it was reported that General Atlantic took the first step toward going public by filing its intention with the SEC. Listing for companies is not only about more liquidity in the market, but also about meeting the need for new capital as they look to diversify into new strategies, such as private debt, and new geographies – a growing trend among major fund managers looking to raise larger and larger vehicles. (Photo by Oren Elbaz on Unsplash)

ALL RIGHTS RESERVED ©