Table of contents

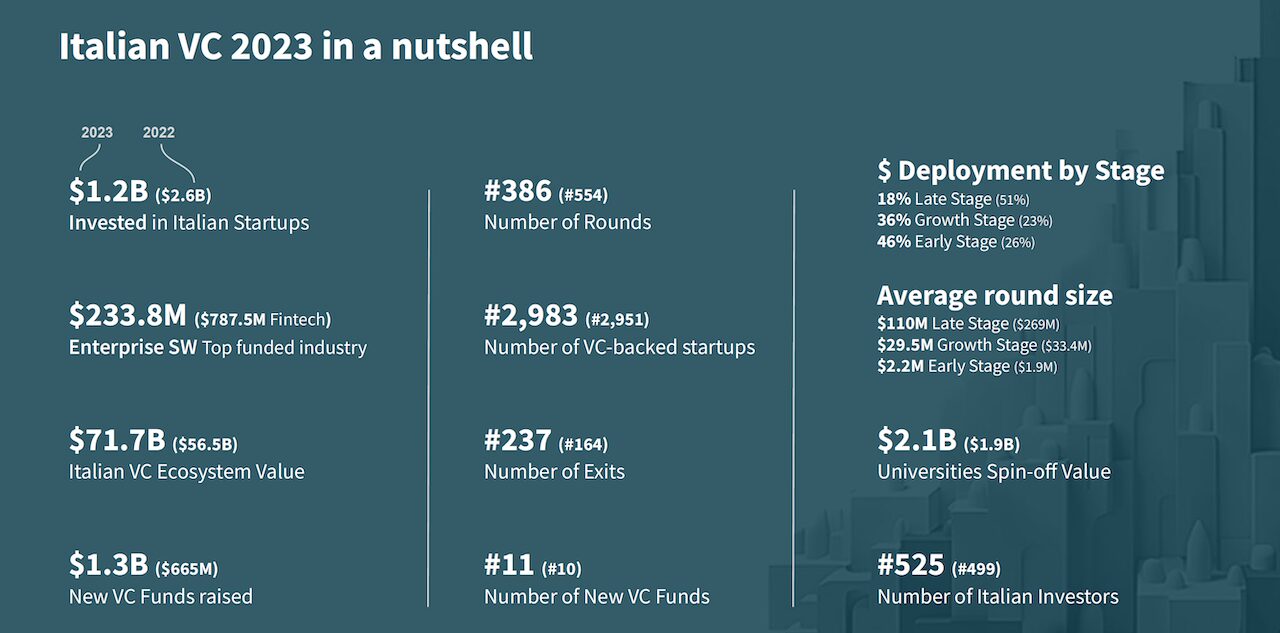

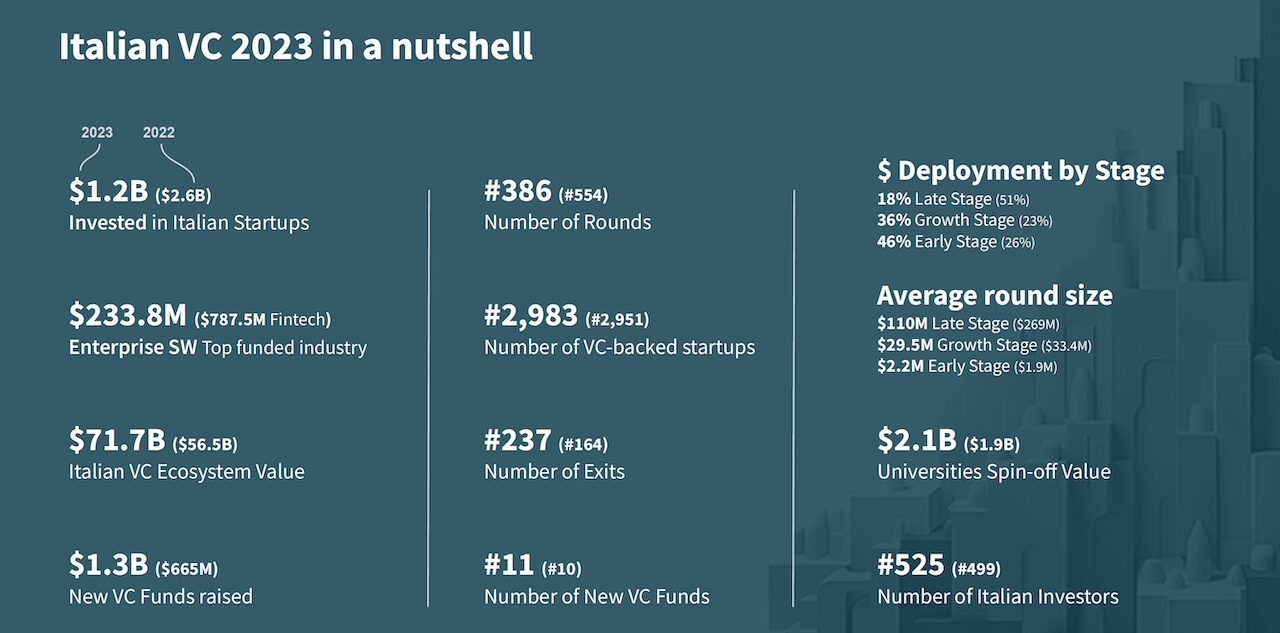

“State of Italian VC” is the report created by P101, an Italian venture capital that invests both in the country and in Europe and which highlights how Italian venture capital in the last 10 years has grown at a significant rate, contributing to the development of the country’s innovation ecosystem. Over the decade, Italian VC has invested a total of about 8 billion euros in startups, through annual investments that have increased from 152.1 million euros in 2013 to 1.1 billion euros in 2023: the figure highlights a robust average growth trajectory (+644%) higher than the European one (+492.5%). In the same period, the number of completed transactions increased from 294 to 387 (+31% vs 80% in Europe), a trend that shows a significant increase in the average size of Italian transactions. 2023 in Italy was characterized by a decline in both investments (-55%) – a widespread trend in Europe (-43% in France, -37% in Spain) – and in the number of rounds (-30% in Italy and Germany, -21% in France and -19% in Spain). Despite this decline, attributable to the macro uncertainties that characterized the year, the overall growth trajectory indicated (+644% over the decade) remains extremely positive. It is also due to these investments that today in Italy there are over 13 thousand startups which, together with about 2000 innovative SMEs (Source: Business Register. The defined sample includes about 15000 companies that include startups and innovative SMEs founded since 2010), in 2023 they generated a production value of over 9.3 billion euros employing about 62 thousand people.  The value of the Italian startup ecosystem, amounting to about 67 billion euros (Enterprise Value), has increased 25-fold in 10 years (more than double the European average), a trend that accelerated in 2023 in which a growth of 27% was recorded (7% in Europe). This growth reflects the scalability of business models and the emergence of companies with potential for further development, especially in the technology sector. The valueof Italian startups in 2023 is still equivalent to that of Spain in 2020, France in 2016 and Germany in 2015, data that highlight a time gap in the development of the ecosystem. However, the increase in the number of startups supported by venture capital in Italy, from 726 in 2013 to 2,983 in 2023 (+271%), charts the course for an acceleration of their development. The average valuation of Italian startups in 2023 exceeded €22 million, after recording the highest compound annual growth rate (+19%) of the decade. Countries such as Germany and France still have average valuations almost double those of Italy, which are still in earlier stages of development, but the data show that a process of maturation is also underway in the Italian ecosystem. Over the past 5 years, VC funds in Europe have raised around €109 billion, down 32% in 2023 (year-on-year). Of these, €3.6 billion was raised in Italy: the country appears not only to be growing significantly (+88% year-on-year), but also to buck the trend compared to Europe. In addition, 2023 also saw a remarkable +71% in the average size of Italian funds. Although the Italian market is growing, it still lags behind more mature ecosystems, but the steady increase in the number of new funds (from 3 in 2019 to 11 in 2023), coupled with the increase in their average size, indicates a market that is deepening and diversifying, suggesting growing investor confidence and a wider range of investment opportunities in the country. “We wanted to carry out an in-depth analysis that would highlight the path taken so far by Italian venture capital and that would allow us to focus on its possible further phase of development,” comments Andrea Di Camillo, founder and managing partner of P101, in a note. The overall growth trajectory of the last decade has been significant, in terms of volumes, investments, creation of innovative companies and impact on the economy: the more than 50 companies in which P101 has invested in the decade, in the same period have generated total revenues of €5 billion and in 2023 alone have employed over 5000 people and generated a turnover of about €1.7 billion. Industry data tell us that the construction of the foundations of the Italian venture capital ecosystem is complete. Now we must look ahead, to the next decade, aware of the road that remains to be taken to make up the gap that still separates us from some European countries, but above all of the challenges that the system will have to face in order to evolve and enter a new phase of maturity, in which the rules of the game will change. Opportunities and competition will increase, with international players looking at our country with growing interest. New drivers, such as artificial intelligence, will change investment trends, which are increasingly focused on services for businesses. The size of funds, investments and startups will increase: companies that have been successful in the past decade are now showing the scalability of their business and are ready to make a dimensional leap that will increasingly take them across borders. And we, venture capital players, will have to lead and not suffer the change towards new business models and offers, without ever forgetting the goal for which the sector was born: to contribute to the development of the Italian innovation ecosystem”. Below, in summary, the main trends related to the evolution of the Italian and European venture capital sector contained in the “State of Italian VC”, a report created by P101 with the support of Dealroom.

The value of the Italian startup ecosystem, amounting to about 67 billion euros (Enterprise Value), has increased 25-fold in 10 years (more than double the European average), a trend that accelerated in 2023 in which a growth of 27% was recorded (7% in Europe). This growth reflects the scalability of business models and the emergence of companies with potential for further development, especially in the technology sector. The valueof Italian startups in 2023 is still equivalent to that of Spain in 2020, France in 2016 and Germany in 2015, data that highlight a time gap in the development of the ecosystem. However, the increase in the number of startups supported by venture capital in Italy, from 726 in 2013 to 2,983 in 2023 (+271%), charts the course for an acceleration of their development. The average valuation of Italian startups in 2023 exceeded €22 million, after recording the highest compound annual growth rate (+19%) of the decade. Countries such as Germany and France still have average valuations almost double those of Italy, which are still in earlier stages of development, but the data show that a process of maturation is also underway in the Italian ecosystem. Over the past 5 years, VC funds in Europe have raised around €109 billion, down 32% in 2023 (year-on-year). Of these, €3.6 billion was raised in Italy: the country appears not only to be growing significantly (+88% year-on-year), but also to buck the trend compared to Europe. In addition, 2023 also saw a remarkable +71% in the average size of Italian funds. Although the Italian market is growing, it still lags behind more mature ecosystems, but the steady increase in the number of new funds (from 3 in 2019 to 11 in 2023), coupled with the increase in their average size, indicates a market that is deepening and diversifying, suggesting growing investor confidence and a wider range of investment opportunities in the country. “We wanted to carry out an in-depth analysis that would highlight the path taken so far by Italian venture capital and that would allow us to focus on its possible further phase of development,” comments Andrea Di Camillo, founder and managing partner of P101, in a note. The overall growth trajectory of the last decade has been significant, in terms of volumes, investments, creation of innovative companies and impact on the economy: the more than 50 companies in which P101 has invested in the decade, in the same period have generated total revenues of €5 billion and in 2023 alone have employed over 5000 people and generated a turnover of about €1.7 billion. Industry data tell us that the construction of the foundations of the Italian venture capital ecosystem is complete. Now we must look ahead, to the next decade, aware of the road that remains to be taken to make up the gap that still separates us from some European countries, but above all of the challenges that the system will have to face in order to evolve and enter a new phase of maturity, in which the rules of the game will change. Opportunities and competition will increase, with international players looking at our country with growing interest. New drivers, such as artificial intelligence, will change investment trends, which are increasingly focused on services for businesses. The size of funds, investments and startups will increase: companies that have been successful in the past decade are now showing the scalability of their business and are ready to make a dimensional leap that will increasingly take them across borders. And we, venture capital players, will have to lead and not suffer the change towards new business models and offers, without ever forgetting the goal for which the sector was born: to contribute to the development of the Italian innovation ecosystem”. Below, in summary, the main trends related to the evolution of the Italian and European venture capital sector contained in the “State of Italian VC”, a report created by P101 with the support of Dealroom.

Evolution of Rounds

Over the decade , Italian venture capital has invested €3.7 billion through early-stage rounds, the annual value of which has increased fivefold, from €102.4 million in 2013 to €515.5 million in 2023. Despite the fact that early-stage investments in 2023 are declining (-28% year-on-year), these rounds remain the backbone of Italian VC (94% in 23 vs 88% in Europe), even if their incidence on total deals is declining (they were 97% in 2019) and is estimated to progressively tend towards the European average (88%). In the face of the decline in the incidence of early-stage investments, the incidence of growth stage rounds is growing, through which about 2.2 billion euros have been invested over the decade. Despite the reduction in the amount invested in 2023 (-26% year-on-year), these have shown the highest growth rate in the last decade (+720%), going from around €50 million in 2013 to over €412 million in 2023. This type of operation is still marginal in Italy (5.6% of the total vs 3% in 19), but their growth in size and the constant consolidation of the sector could progressively bring their incidence towards the European average (10.4% of the total). Late-stage rounds continue to be rare in Italy: the annual value has risen from 0 to 205 million euros over the decade during which only 12 transactions have been carried out. These have been concentrated in the last 5 years during which a total of about 2 billion euros have been invested, an amount that includes the peak of 1.2 billion euros in 2022.

Sectors

2023 was characterized by a recalibration of investments from sectors that experienced explosive growth during the pandemic, such as fintech (€127.5 million in 23 vs €732.8 million in 22) and healthcare (€122.8 million in 23 vs 324.3 million in 22), towards emerging and sustainable technologies such as space (€134 million) and energy (€147 million). Business software, which has always been at the center of investors’ attention, rises to first place in the Italian ranking (217.7 million euros in 23). Investments in startups linked to the sustainable development goals (SDGs), amounting to €120 million in 2023, grew 1.6 times compared to 2019, but remain far from the peak of 2022 (€250 million). In 2023, investments in B2B startups also increased significantly, accounting for 82% of the total (they were 54% in 2021), growth consistent with the digitization trend of companies. The concentration of investments remains high: the top 5 sectors subject to investment in Italy account for more than 50% of total funding, and the top 10 account for over 80%.

Exit

As the ecosystem has evolved, exits have also increased significantly over the decade. In particular, those made through M&A have grown exponentially , both in terms of the number of acquisitions, which increased 16 times in the decade with an all-time peak of 234 in 2023 (+47% on 22), and in the number of buyouts (which grew 10 times over the decade). Italian IPOs show modest and fluctuating activity, contrary to a more dynamic European landscape. The IPO market for venture-invested companies in Italy is even more static: in 2023, there were only three IPOs of companies supported by venture capital with a digital focus.

Investors

Italian investors continue to account for the vast majority of domestic venture capital (69% in 2023). From 2020 onwards, there has been a growing presence of European and North American investors, from 10% and 5% respectively in 2020 to 19% and 8% in 2023. Investors from Asia and the rest of the world had minimal and fluctuating involvement. The data confirm a correlation between the size of the rounds and the presence of foreign investors, partly due to the small average size of Italian venture capital funds and the limited number of domestic funds focused on the late stage phase.

Evolution of the ecosystem

The Italian innovation ecosystem is developing strongly: in the last five years, the value of Italian university spin-offs (incubators, accelerators and venture capital networks) has quadrupled, and in 2023 the 907 registered spinoffs reached a value of about 2 billion euros. The European programmes Horizon 2020 and Horizon Europe have been an important source of grants for universities in Italy. From 2014 to 2023, around 7,500 Italian university projects received a total of €2.83 billion. This trend is expected to continue, contributing significantly to the country’s economic growth and technological advancement. The full version of the “State of Italian VC” report is available at this link

ALL RIGHTS RESERVED ©