Table of contents

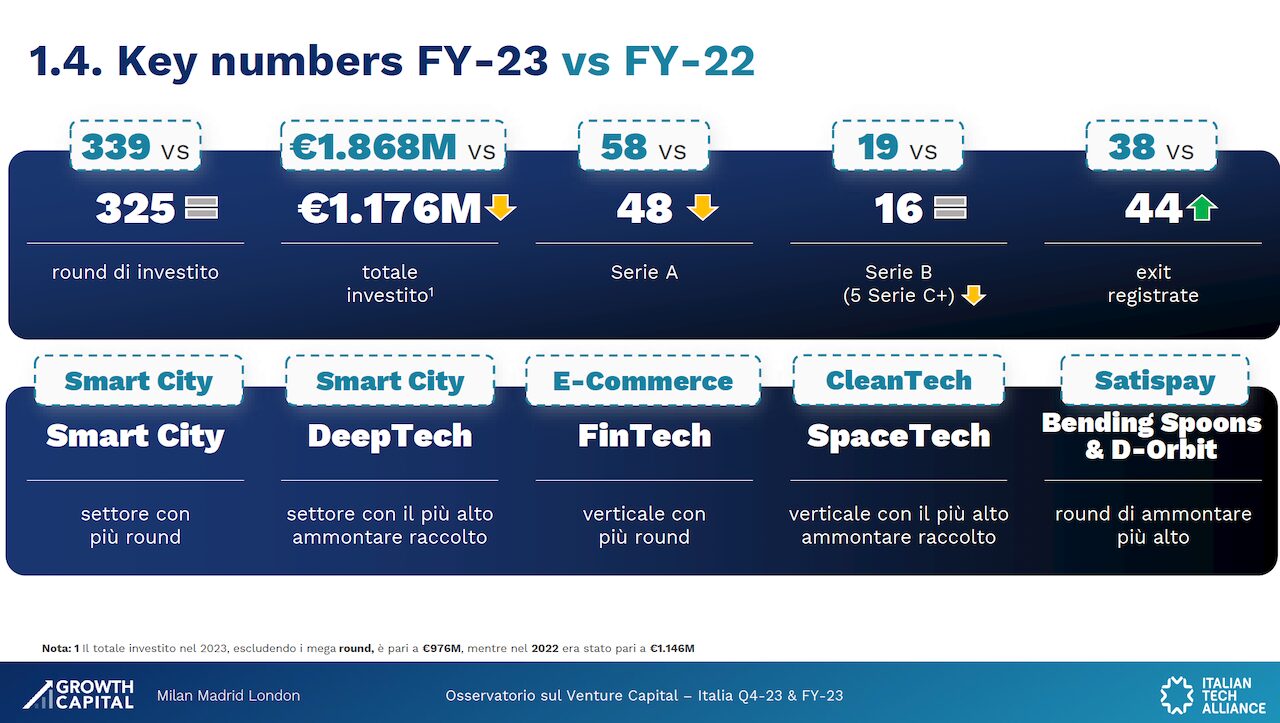

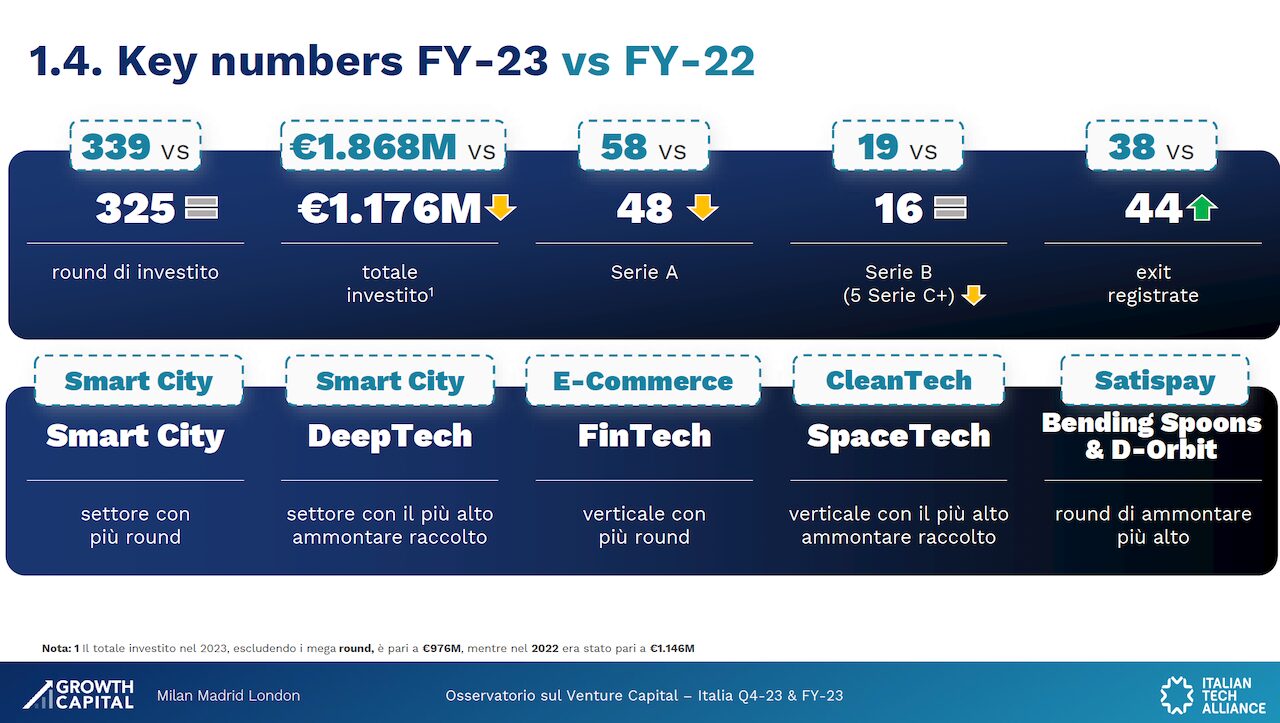

In 2023, investments in startups and innovative companies in Italy amounted to €1.176 billion in 325 funding rounds, recording a decrease in the amount invested of 37% compared to the previous year when they were €1.868 billion. The decline is mainly due to the lower incidence of mega rounds (17% vs 38%) with the number of rounds essentially stable (339 in 2022 and 325 in 2023). Smart city is the sector with the highest number of rounds, while deeptech is the one with the highest amount raised. This is the summary picture that emerges from the Observatory on venture capital in Italy, created by Growth Capital, in collaboration with Italian Tech Alliance. The observatory, now in its third year, monitors the quarterly performance of investments and trends in the Italian venture capital ecosystem.

Italy Analysis

The €383 million in premiums made Q4 the best quarter since Q3-22, highlighting a growth trend over the course of the year. The fourth quarter was also the second-best ever in terms of number of rounds (90), up from previous rounds and above the historical average. While ecosystem indicators return to levels comparable to 2021, down from the peak of 2022, the evolution recorded over the last six years still shows the constant and progressive maturation of the Italian ecosystem.  Looking at the full year, in 2023 there was a slowdown in activity compared to the record values of 2022 and closed with 1.17 billion euros invested (-37% compared to 2022 in terms of amount raised and -4% number of deals). The decrease in investments is largely attributable to the lower incidence of mega rounds (17% vs 38%), excluding which 2023 (976 million) is slightly lower than 2022 (1.14 billion) and higher than 2021 (895 million). In 2023, the Italian VC returned to the slower and steady maturation trajectory that began in 2019, which can be seen in the improvement of fundamental metrics such as the number of exits, the participation of international investors and the median amount of rounds. Considering the segmentation of the rounds by type, in Italy in Q4-23 pre-seed and seed are the most frequent type (23 and 64 million respectively raised, with 32 and 42 rounds), while the Series B and subsequent rounds cover 66% of the amount, for a total of 254 million in 7 rounds. In the whole of 2023, on the other hand, almost half of the rounds were seed (257 million raised in 164 rounds), while the 348 million of Series A make it the type that raised the most capital, in 48 funding rounds. The significant increase in the number of early-stage active investors, including the vertical accelerators promoted by CDP, led to strong growth in the number of pre-seed rounds (92 in 2023 compared to 55 in 2022). The analysis by sector shows that in Q4 deeptech and software totaled the highest number of rounds – 15 and 13 – followed by food & agriculture with 12, while at the annual level smart cities prevail with 48, followed by deeptech (45) and software (42). Looking at the amount raised, in Q4 we still find deeptech in the lead, with 127 million, followed by life sciences with 79 and food & agriculture with 61. With 251 million, deeptech also leads the ranking in 2023, followed by software with 199 million and life science with 186 million. Software and smart cities have historically been the sectors that have seen the most rounds, while fintech is the sector that has historically raised the most, followed by smart cities. Another element that emerges is that the average size of rounds is growing in the deeptech and media sectors, while it is falling in fintech and digital. Among the top 5 deals in 2023,

Looking at the full year, in 2023 there was a slowdown in activity compared to the record values of 2022 and closed with 1.17 billion euros invested (-37% compared to 2022 in terms of amount raised and -4% number of deals). The decrease in investments is largely attributable to the lower incidence of mega rounds (17% vs 38%), excluding which 2023 (976 million) is slightly lower than 2022 (1.14 billion) and higher than 2021 (895 million). In 2023, the Italian VC returned to the slower and steady maturation trajectory that began in 2019, which can be seen in the improvement of fundamental metrics such as the number of exits, the participation of international investors and the median amount of rounds. Considering the segmentation of the rounds by type, in Italy in Q4-23 pre-seed and seed are the most frequent type (23 and 64 million respectively raised, with 32 and 42 rounds), while the Series B and subsequent rounds cover 66% of the amount, for a total of 254 million in 7 rounds. In the whole of 2023, on the other hand, almost half of the rounds were seed (257 million raised in 164 rounds), while the 348 million of Series A make it the type that raised the most capital, in 48 funding rounds. The significant increase in the number of early-stage active investors, including the vertical accelerators promoted by CDP, led to strong growth in the number of pre-seed rounds (92 in 2023 compared to 55 in 2022). The analysis by sector shows that in Q4 deeptech and software totaled the highest number of rounds – 15 and 13 – followed by food & agriculture with 12, while at the annual level smart cities prevail with 48, followed by deeptech (45) and software (42). Looking at the amount raised, in Q4 we still find deeptech in the lead, with 127 million, followed by life sciences with 79 and food & agriculture with 61. With 251 million, deeptech also leads the ranking in 2023, followed by software with 199 million and life science with 186 million. Software and smart cities have historically been the sectors that have seen the most rounds, while fintech is the sector that has historically raised the most, followed by smart cities. Another element that emerges is that the average size of rounds is growing in the deeptech and media sectors, while it is falling in fintech and digital. Among the top 5 deals in 2023,

Bending Spoons

(100 million, growth VC) and

D-Orbit

(100 million, series C) are in the lead, followed by Nouscom (67.5, series C). Fourth position for

Aavantgarde Bio

(61 million, series A) and, following,

Energy Dome

(55 million, series B). In 2023, the number of active investors decreased compared to 2022 and grew slightly compared to 2021, with 35% of active investors in the year coming internationally. In addition, the Observatory shows that an international investor was present in each of the most substantial rounds. CDP Venture Capital remains the most active investor in 2023, with 52 deals, followed by Exor Seeds/Vento Ventures with 24 and Azimut with 21. Finally, 2023 marks an all-time high in terms of exits, which were 44 (41 M&A transactions and 3 IPOs), recording a growth of 16% compared to 2022. The update of the VC index, created by Growth Capital in collaboration with Italian Tech Alliance, was also presented. It is an indicator on a scale of 1 to 10 calculated every six months and which provides an indication of the stage of development of the VC ecosystem in Italy and the sentiment of its players. The index is constructed by considering quantitative inputs, from market data analysis, and qualitative inputs, provided by VC operators (startups and investors) based on the sentiment of the current and prospective situation.

Europe Analysis

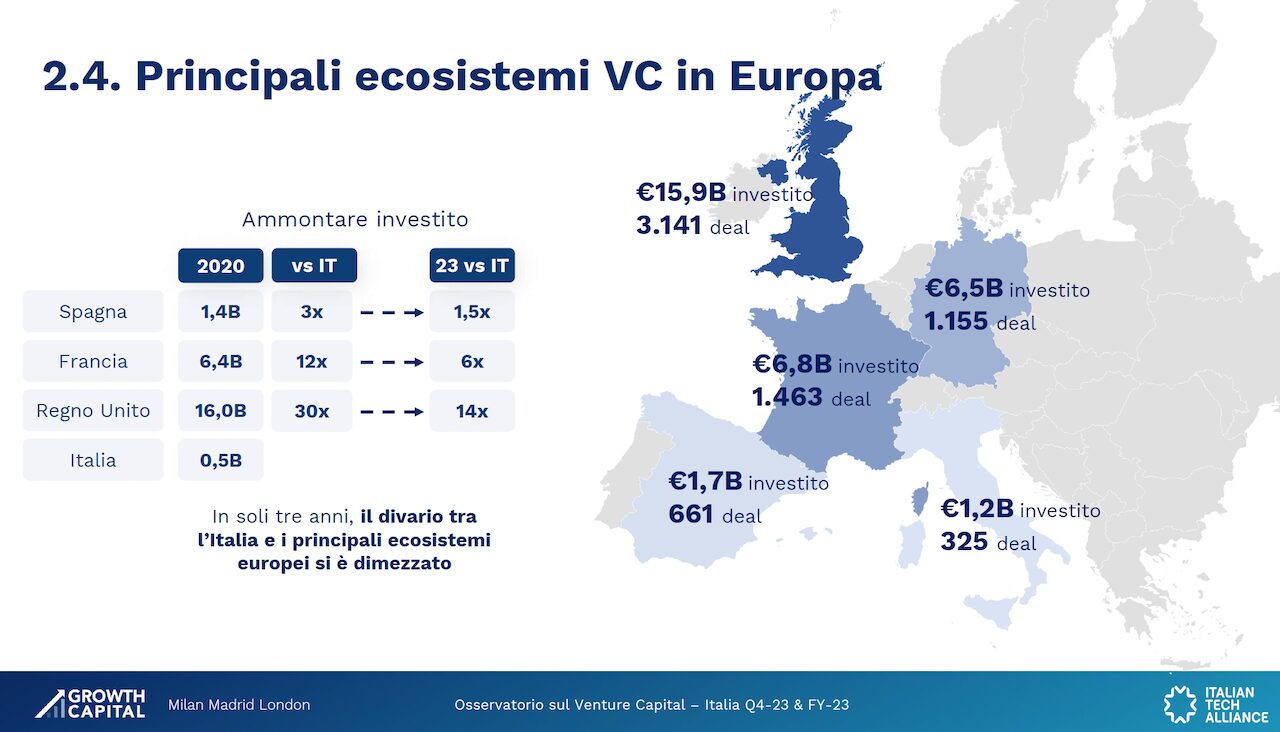

With €55 billion raised in 10,740 rounds, 2023 is comparable to 2020 levels, far from 2021 (-48%) and 2022 (-44%). Considering Q4-23 alone, €13 billion was raised in 2,327 rounds, respectively -22% and -5% compared to Q3-23. Looking at the ecosystem in Spain, with €1.7 billion raised in 668 rounds, 2023 closes down 50% in amount raised and 32% in number of rounds compared to 2022. While in France, €6.8 billion was raised in 1,463 rounds – 2023 closes down 32% in amount raised and 25% in number of rounds compared to 2022. In the UK, €15.9 billion was raised in 3,141 rounds – 2023 closes down 52% in amount raised and 40% in number of rounds compared to 2022.  “After a 2022 characterized by a particularly favorable market phase, Italian venture capital in 2023 followed a more contained and steady maturation trajectory, which began in 2019, recording significant improvements in fundamental metrics, such as the number of exits, the participation of international investors and the median amount of rounds. We expect that in 2024 investments will exceed those of 2023, with possible positive developments related to the number and characteristics of mega rounds and the participation of international investors in the Italian VC, which we believe could be significant. This outlook is also supported by the forecast of an increase in the number of late-stage rounds. For example, among companies that completed a Series A between 2020 and 2022, only 29% completed a new fundraiser, while a considerable number could do so in the next 18 months. On the contrary, we expect IPOs to continue to be marginal,” Fabio Mondini de Focatiis, founding partner at Growth Capital, said in a note. “The Observatory highlights how in 2023 investors focused on areas that have a real and concrete impact on improving people’s living conditions, such as life science,” explains Francesco Cerruti, general manager of Italian Tech Alliance. Another area that arouses strong interest is that of activities related to sustainable development, which is well suited to the destination of the resources made available by the PNRR. Despite the undeniable drop in absolute numbers compared to 2023, the Observatory paints a positive picture, especially if we take into account the sharp decrease in the distance that separates the Italian ecosystem from that of other leading countries at the European level”. The full report and research methodology are available at this link.

“After a 2022 characterized by a particularly favorable market phase, Italian venture capital in 2023 followed a more contained and steady maturation trajectory, which began in 2019, recording significant improvements in fundamental metrics, such as the number of exits, the participation of international investors and the median amount of rounds. We expect that in 2024 investments will exceed those of 2023, with possible positive developments related to the number and characteristics of mega rounds and the participation of international investors in the Italian VC, which we believe could be significant. This outlook is also supported by the forecast of an increase in the number of late-stage rounds. For example, among companies that completed a Series A between 2020 and 2022, only 29% completed a new fundraiser, while a considerable number could do so in the next 18 months. On the contrary, we expect IPOs to continue to be marginal,” Fabio Mondini de Focatiis, founding partner at Growth Capital, said in a note. “The Observatory highlights how in 2023 investors focused on areas that have a real and concrete impact on improving people’s living conditions, such as life science,” explains Francesco Cerruti, general manager of Italian Tech Alliance. Another area that arouses strong interest is that of activities related to sustainable development, which is well suited to the destination of the resources made available by the PNRR. Despite the undeniable drop in absolute numbers compared to 2023, the Observatory paints a positive picture, especially if we take into account the sharp decrease in the distance that separates the Italian ecosystem from that of other leading countries at the European level”. The full report and research methodology are available at this link.

ALL RIGHTS RESERVED ©