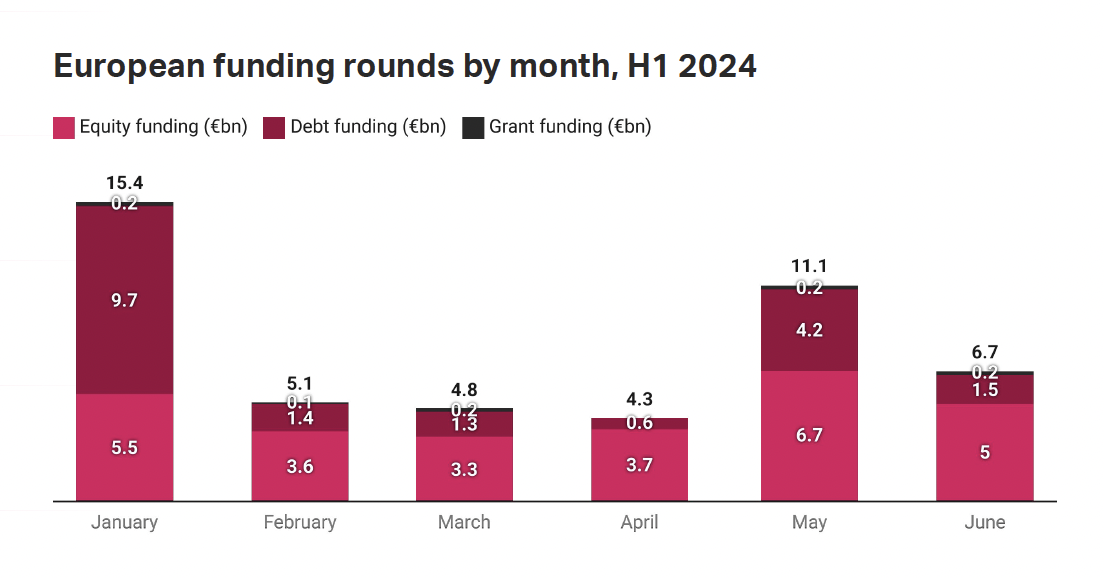

European start-ups raised EUR 47.3 billion in 2,971 deals in the first half of the year, according to data collected by Sifted and published in the H1 2024 report.

Equity-based transactions totalled EUR 27.8 billion in H1 2024, down from the previous half-year but up from the same period last year. Debt operations in the first half of the year totalled EUR 18.7 billion from 92 operations, setting a new annual record for European debt financing.

Fundraising for early stage start-ups, i.e. pre-seed, seed and Series A, accounted for 82.8% (2,460) of total deals in the first half of the year, but only 19.7% (EUR 9.3bn) of the deal volume.

In the first half of the year, 87 rounds of over USD 100 million were announced, of which 63 were equity-based, the highest figure since the first half of 2022.

The climate technology sector received by far the most investment between January and June (EUR 21.3 billion) thanks to a handful of giant debt transactions. In the second quarter, however, fintech outperformed climatech.

Swedish climate-tech companies Northvolt (EUR 5 billion) and H2 Green Steel (EUR 4.75 billion) raised the most capital in Q1, followed by London-based card reader manufacturer SumUp (EUR 1.5 billion). The Parisian start-up H, specialised in AI, obtained the largest early-stage deal (EUR 203.3 million).

The UK recorded the highest volume in the first half-year (EUR 13.3 billion), just ahead of Sweden (EUR 12 billion) thanks to a record May. France came third, hosting EUR 6 billion worth of transactions.

The unicorns are on the upswing: Europe created eight new $1 billion companies in the first half of the year, more than in the whole of 2023.

Energy storage, advanced materials and electric vehicles were the most important segments by volume of transactions in the first half of the year, while biotechnology, medical technology and data and analytics achieved the highest number of transactions.

Stockholm-based start-ups (EUR 10.8 bn) received the most funding, mainly thanks to Northvolt and H2 Green Steel, followed by London-based start-ups (EUR 10.3 bn). Grenoble (EUR 1.3 billion) surprisingly appears in 5th place in the ranking of the best cities in terms of half-year results.

Accelerator Antler was the most active investor in Europe in the first half of the year with 82 investments, followed by SFC Capital (78). The European Investment Bank carried out the largest number of debt financing operations with 7.

European venture capital companies have raised more than EUR 15 billion in new capital, the most since the first half of 2022.

Jonathan Sinclair, head of research at Sifted says in a note: ‘The European technology ecosystem is probably in a better situation than it was six months ago. EUR 47.3 billion, which includes EUR 18.7 billion in debt financing, was injected into European start-ups in the first half of the year. Equity funding is down about 8 per cent from the second half of 2023, but the shoots of recovery are solid and Europe is finding a new normal after years of volatility. In particular, venture debt has become mainstream and is helping to offset the slight decline in equity financing, secondaries are improving investor liquidity, climate technology is booming and fintech is back, almost, after 18 months of crisis.”

The Sifted H1 2024 report can be downloaded in full at this link

ALL RIGHTS RESERVED ©