Table of contents

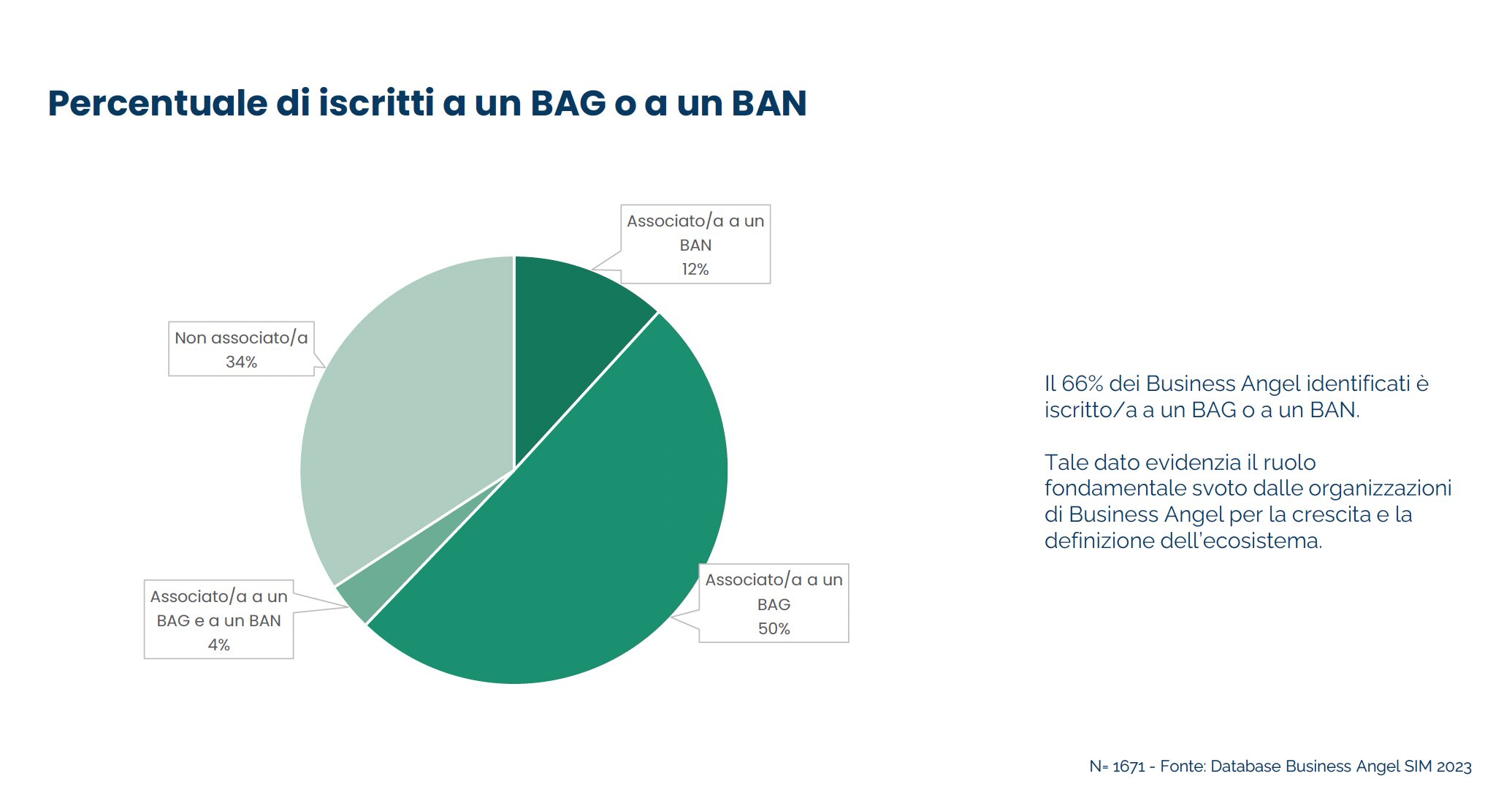

There are over 1600 business angels active in Italy, 66% of which are registered with at least one of the 33 existing business angel groups (BAG) and business angel networks (BAN) that in the period 2018-2022 participated in more than 120 funding rounds, for an invested amount of over 45 million euros. These are the numbers that emerge from the report “Business angel in Italy: the impact of angel investing”, carried out by Growth Capital in collaboration with Italian Tech Alliance and with the Social Innovation Monitor of the Politecnico di Torino and the University of East Anglia (UEA). The research was also supported by the main companies active in Italy in angel investing. The analysis was carried out with the aim of outlining an up-to-date mapping at national level of business angels and the organizations that bring them together; analyze the distinctive characteristics of Italian business angels; highlight the impact on startups deriving from funding rounds in which business angel organizations participated and propose regulatory interventions in favor of angel investing, with the ultimate aim of supporting the development of the Italian innovation ecosystem.

Who are business angels?

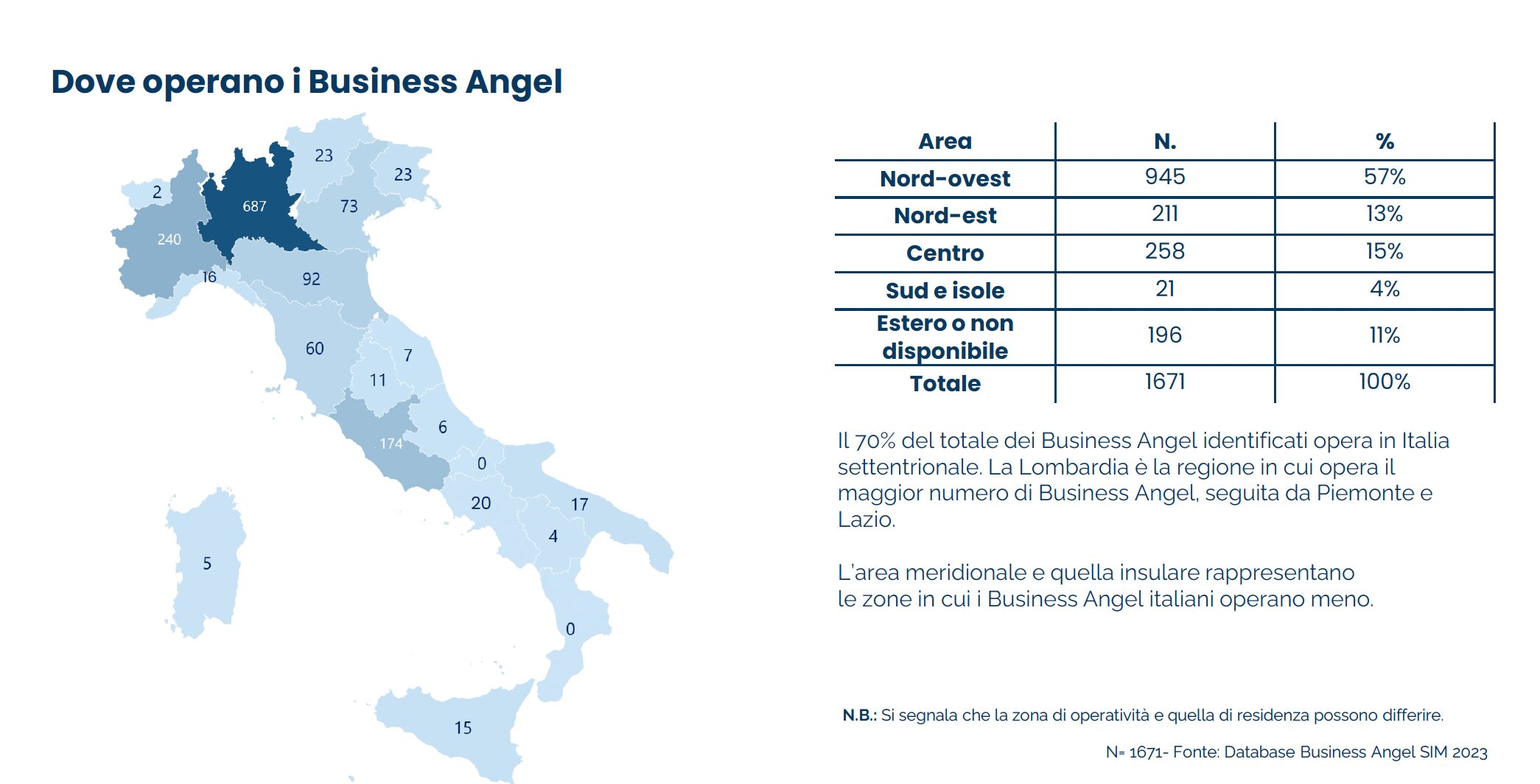

70% of the total number of business angels identified operate in northern Italy: Lombardy is in the lead with 687 active entities, followed by Piedmont with 240 and Lazio with 174. 94% of the mapped business angels have a higher education degree, and 78% have an entrepreneurial or managerial background. In addition, it is important to note that 66% of business angels are members of a business angel group (BAG) or a business angel network (BAN), confirming the fundamental role played by business angel organizations in the growth of the ecosystem. Specifically, there are 17 business angel groups operating in Italy (11 in the North-West, 4 in the North-East and 2 in Central Italy) and 16 business angel networks (7 in the North-West, 2 in the North-East, 5 in Central Italy and 2 in the South and Islands).

The activity of angel investing

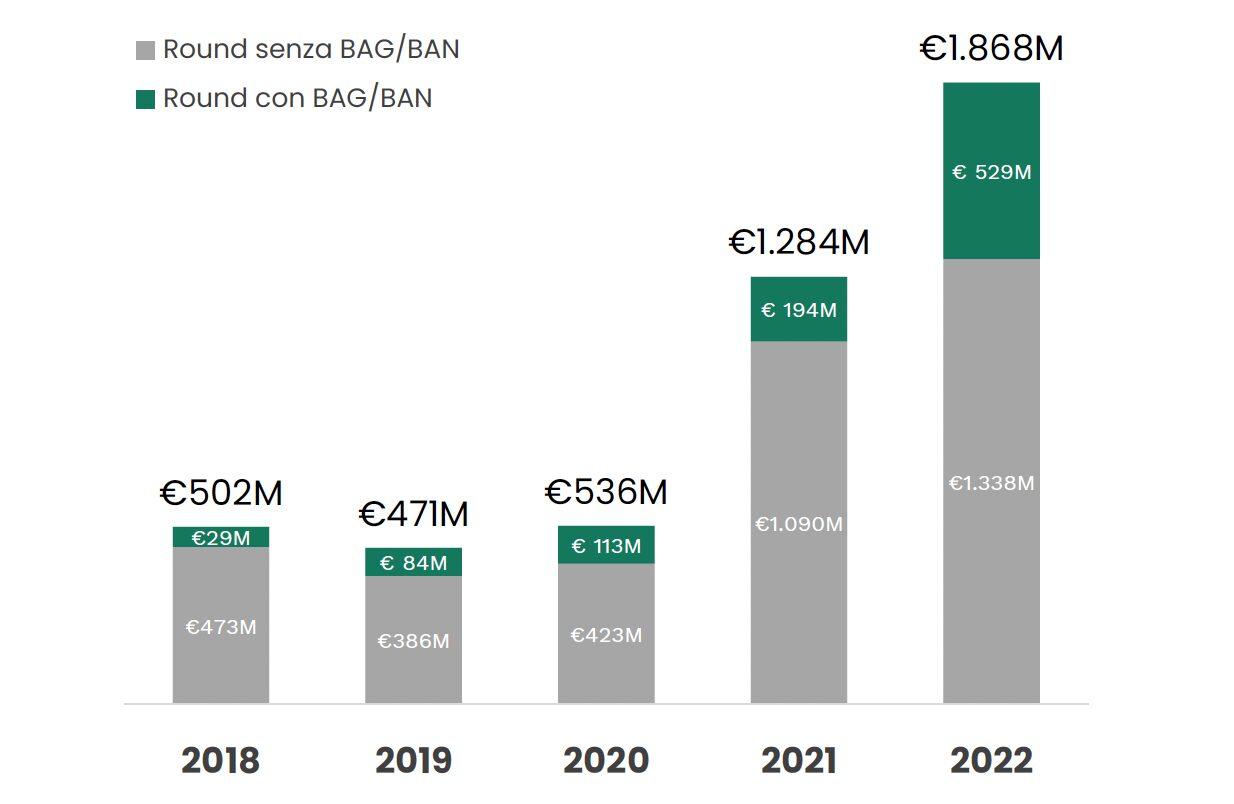

In the last five years, about 10% of the investment rounds completed in Italy have seen the participation of one or more BAG/BAN, with fluctuations from 9% to 13% of the total, with a progressive and continuous growth from the 20 rounds in 2018 involving BAG or BAN to the 30 in 2022. Looking at the 2018-2022 period, it should also be noted that the amount invested in rounds with the presence of BAG/BAN represented about 20% of the total invested in Italy, with fluctuations from 6% to 28%. In fact, the amount invested in rounds with the presence of BAG/BAN represented a steadily increasing portion of the total invested, rising from €29 million in 2018 (out of total investments of €502 million) to €529 million in 2022 (out of over €1.8 billion of investments). When participating in a capital increase, BAG/BAN covers on average about 5% of the amount invested, a percentage that reaches about 10% if mega rounds (i.e., rounds of €100 million or more) are excluded. As far as the number of rounds is concerned, the report highlights how seed rounds represent the preferred stage of maturity for BAG/BAN. The presence of BAG/BAN is also interesting in more advanced investment stages (Series A and B+), typically attributable to follow-ons on companies that had already been invested previously. Looking at the sectors, in the period covered by the analysis, BAG and BAN invested mainly in companies in the digital (27 rounds), life sciences (25), fintech (17) and smart city (16) sectors. Lombardy, Piedmont and Lazio are the most represented reasons both in terms of number of rounds and amount invested. The report also highlights how companies in which BAG or BAN have invested have grown faster than companies “without BAG/BAN”, both in terms of turnover and in terms of number of employees, confirming the importance for innovative startups and SMEs to raise smart money from investors. In particular, comparing the 2018 and 2021 financial statements for companies that closed at least one funding round in that four-year period, it emerged that the median growth in terms of turnover was more than 400% among companies that received capital from a BAG/BAN, while only 190% among companies that closed a round without a BAG/BAN. Looking at the median values, these differences also emerged with respect to the number of employees (+120% between companies with BAG/BAN and +100% without). The results were even more marked in terms of EBITDA (+120% with BAG/BAN and +20% without) and in terms of intangible assets (+350% with BAG/BAN and +290% without), demonstrating on the one hand greater management control and above all a greater drive for innovation in companies with a BAG/BAN among investors. “Through this research we have contributed to the analysis of the impact of investments by business angels, a category that is fundamental for the growth of the sector in Italy,” comments Fabio Mondini de Focatiis, founding partner of Growth Capital, in a note. Among the results that emerged, we note that, comparing the 2018 and 2021 data relating to companies that concluded at least one round of funding in the four-year period 2018-2021, there is a median increase of more than five times the turnover in companies financed by an BAG/BAN, compared to an increase of less than three times for companies that closed a round without a BAG/BAN”.  “This study is important because it clearly shows how year after year in Italy the weight of angel investing has grown in supporting the growth of startups and innovative companies – explains Francesco Cerruti, general manager of Italian Tech Alliance – . Business angels are now recognized as key elements in raising capital to support the growth of small and young businesses, particularly seed and early stage rounds, which are less covered by traditional VCs than investment rounds at more advanced stages. As an association that represents all investors in innovative companies, Italian Tech Alliance will continue to work to ensure that innovative actions and interventions are promoted both at national and EU level to support this type of investor. In particular, it would be desirable to provide tax advantages in the event of an exit, in special cases to provide for exemption from the holding period constraint and, as is already the case in the United Kingdom, to provide for a differentiation of the benefits depending on the business angel’s investment ticket and the size of the capital increase”. “In accordance with the research carried out by SIM in recent years, the Italian angel investing ecosystem has shown resilience and capacity for growth. However, there are still many issues to be explored and many actions to be taken to facilitate greater growth of this important resource for our economy. The benefits of supporting female angel investing, a growing role of impact investing and the advent of new players and new technologies in the ecosystem are some of the main opportunities that business angels are and will increasingly have to be able to seize. Research like ours can shed light on these changes and suggest ways to deal with them,” he says Davide Viglialoro, scientific director of the research. The full report and research methodology are available at this link.

“This study is important because it clearly shows how year after year in Italy the weight of angel investing has grown in supporting the growth of startups and innovative companies – explains Francesco Cerruti, general manager of Italian Tech Alliance – . Business angels are now recognized as key elements in raising capital to support the growth of small and young businesses, particularly seed and early stage rounds, which are less covered by traditional VCs than investment rounds at more advanced stages. As an association that represents all investors in innovative companies, Italian Tech Alliance will continue to work to ensure that innovative actions and interventions are promoted both at national and EU level to support this type of investor. In particular, it would be desirable to provide tax advantages in the event of an exit, in special cases to provide for exemption from the holding period constraint and, as is already the case in the United Kingdom, to provide for a differentiation of the benefits depending on the business angel’s investment ticket and the size of the capital increase”. “In accordance with the research carried out by SIM in recent years, the Italian angel investing ecosystem has shown resilience and capacity for growth. However, there are still many issues to be explored and many actions to be taken to facilitate greater growth of this important resource for our economy. The benefits of supporting female angel investing, a growing role of impact investing and the advent of new players and new technologies in the ecosystem are some of the main opportunities that business angels are and will increasingly have to be able to seize. Research like ours can shed light on these changes and suggest ways to deal with them,” he says Davide Viglialoro, scientific director of the research. The full report and research methodology are available at this link.

ALL RIGHTS RESERVED ©