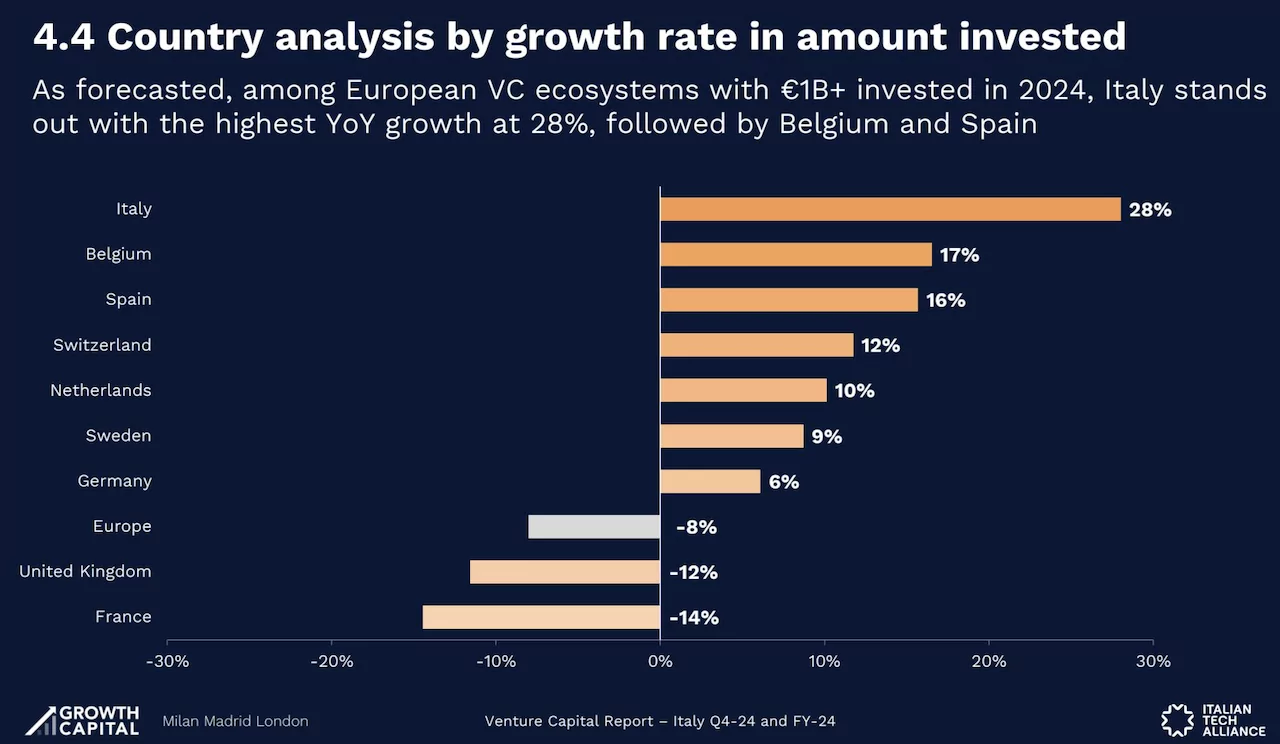

One and a half billion euros, equal to a growth of 28%, the highest in Europe and bucking the European figure (which we wrote about here ), is the total amount of investments in start-ups and scaleups in Italy in 2024. The figure emerges from Growth Capital and Italian Tech Alliance’s quarterly report, which punctually tracks the sector’s performance and, as the year begins, publishes data for both the fourth quarter and the entire previous year.

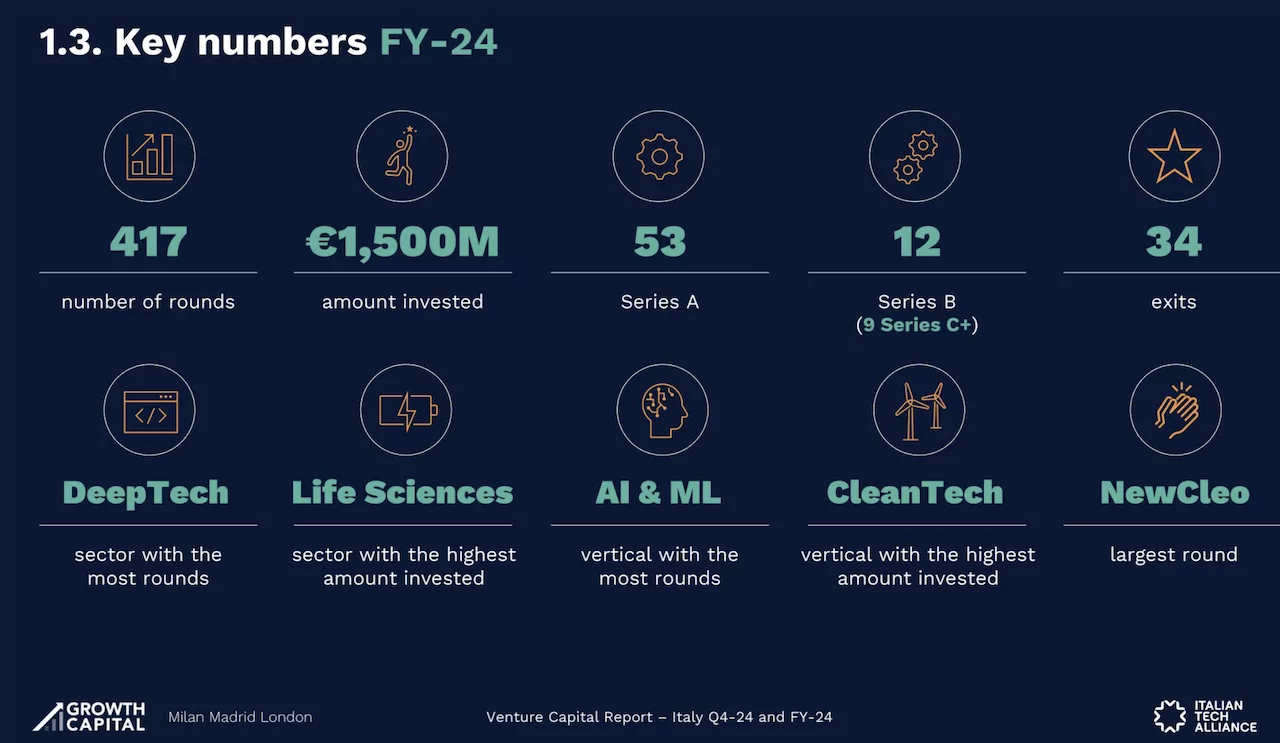

The EUR 1.5 billion is spread over 417 investment rounds, also up 31% from 2023, confirming 2024 as the best year for number of rounds. As predicted in previous editions of the Observatory, among European VC ecosystems with more than one billion invested in 2024, Italy stands out with the highest annual growth. Deeptech is the sector with the highest number of rounds while lifescience is the one with the highest amount raised. In 2024, Italy saw the launch of 15 new funds for a total of EUR 1.4 billion currently raised, while 297 investors were active in the Italian market, of which 42% came from abroad, confirming how Italian start-ups are increasingly on the radar of international investors, a trend that has been growing for a few years now.

The presentation of numbers relating to investments in startups and scaleups in 2024 was commented by Francesco Cerruti, managing director of Italian Tech Alliance, Fabio Mondini de Focatiis and Giacomo Bider, respectively founding partner and senior associate of Growth Capital, Giuseppe Donvito partner of P101 and president of Italian Tech Alliance, Davide Turco co-founder and managing director Indaco Venture Partners, Elisabeth Rizzotti co-founder and COO – managing director Italy of Newcleo, and Alessio Cantore co-founder and chief scientist of Genespire and researcher at SR-Tiget.

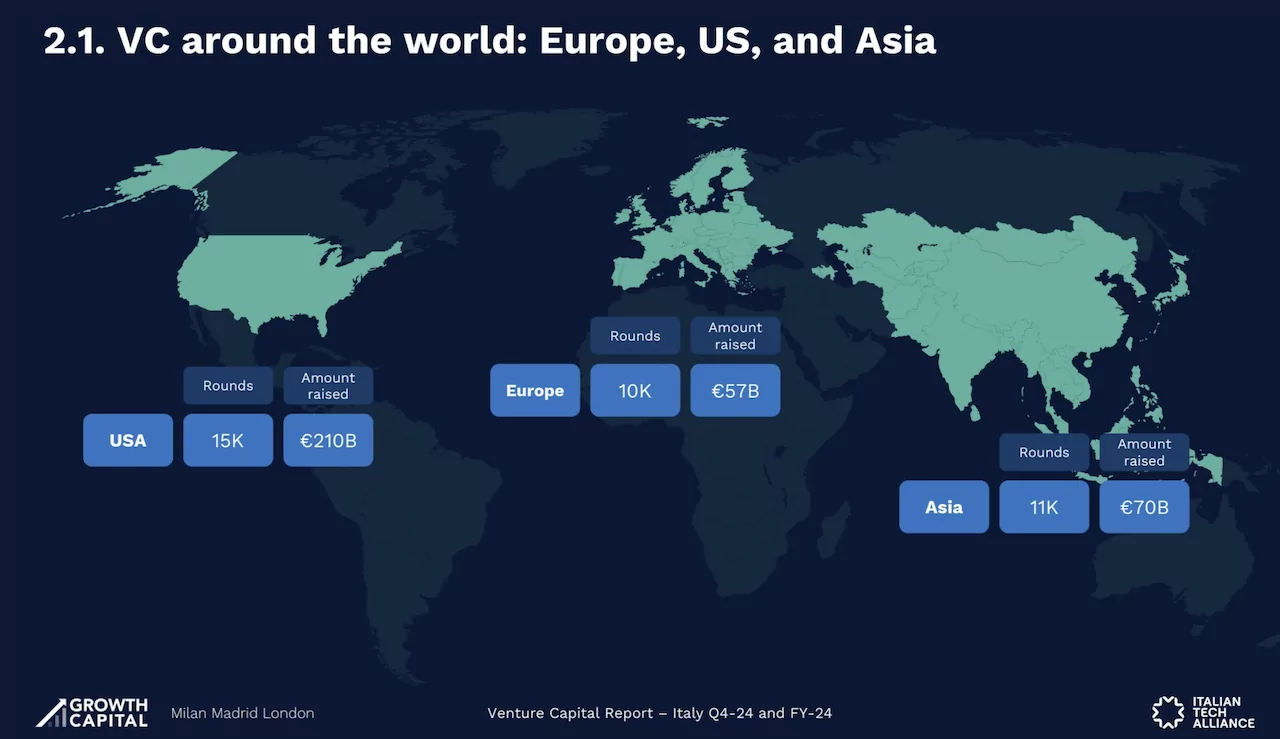

The Italian figure is part of the international scenario that saw 15,260,000 rounds close in 2024 in the USA, for a collection of $210 billion; in Asia, there were 11,000 rounds for $70 billion invested, while Europe saw the closure of 9,600 rounds for €57 billion in investments. Looking at Italy, with EUR 1.5 billion raised in 417 rounds, 2024 was the best year in terms of number of rounds and the second best after 2022 in terms of amount. The Italian ecosystem recorded the highest year-on-year growth in 2024 (+28%), followed by Belgium (+17%) and Spain (+16%), in a scenario that saw Europe decline by 8%, and the UK and France markets decline by 12% and 14% respectively.

Considering the segmentation of rounds by type, in Italy in 2024 pre-seed, seed and bridge account for 82% of all rounds (up from 78% in 2023). The incidence of late-stage rounds on the total harvest (43%) is returning to pre-2023 levels. In detail, there were 142 pre-seed rounds with €64m invested, seed 152 (€209m), bridge 49 (€114m), series A 53 (€459m), series B 12 (€232m) and series C+ 9, for €422m investment.

The analysis by sectors sees deeptech in the lead with 64 rounds, followed by software, lifescience and smart city, with 63, 62 and 61 rounds respectively. Fifth position for food & agriculture, with 43 rounds. Looking at what has happened over the past five years, there has been significant growth in deals in the deeptech, software and lifescience sectors, driven by the activity of accelerators and incubators focused on these sectors. Looking instead at the amount raised, 2024 sees lifescience on the podium with 300 million euro, followed by smart city with 296 and software with 262; followed by fintech with 175 million and deeptech with 163. Looking at the last five years, the food & agriculture and digital sectors have seen a decrease in capital raised, while software has seen a steady increase over time.

The top five deals in 2024 are led by Bending Spoons (144 million, growth VC), followed by Newcleo (135 million, Series A), MMI (101 million, Series C), Satispay (60 million, growth VC) and D-Orbit (50 million, Series C).

In 2024, there were 297 active investors in Italy, in line with the last two years. 42% of these come from abroad (they were 35% in 2023). Since 2020, 208 different international investors have participated in Italian rounds, mainly from the UK, Germany, France and Switzerland. The participation of international investors continues to be prominent in the largest funding rounds, although 2024 marked an increase in their presence in rounds of all sizes. Consistent with 2023, CDP Venture Capital, Azimut and Vento Ventures are the three most active investors in the Italian VC ecosystem.

On the exit front, 2024 was a complex year, with a reduced number of deals (34, compared to 43 in 2023) and a decrease in overall value compared to the previous year. Exits were mainly attributable to M&A deals, with only one IPO recorded.

During the event, the VC Index was also presented. This is an indicator on a scale of 1 to 10 calculated every six months and provides an indication of the stage of development of the VC ecosystem in Italy and the sentiment of its players. The index is constructed by considering quantitative inputs, from market data analysis, and qualitative inputs, provided by VC operators (startups and investors) based on the sentiment of the current and prospective situation.

“In 2024, while Europe saw results in line with the previous year, the resilience and momentum of the Italian VC ecosystem confirmed its path to greater maturity. Italy set a record in the number of deals, albeit with many confidential rounds, and saw a 28% year-on-year increase in the amount invested, establishing itself as the fastest growing market among comparable markets, as per our forecasts. In 2024, the announcement of new VC funds totalling around EUR 1.4 billion brought the level of dry powder to unprecedented levels. Looking ahead to 2025, we expect an increase in both the number of deals and the amount invested, excluding mega rounds, whose frequency and size remain difficult to predict. This growth will be driven mainly by the high availability of capital, the increased participation of international investors and the growth in size of Italian VC funds,’ says Fabio Mondini de Focatiis .

“The numbers of the Observatory tell us that 2024 was a year of consolidation for the Italian innovation ecosystem, which, thanks also to the important innovations introduced at the policy level, will be able to grow further in 2025, reducing the gap with other European countries. The big challenges for 2025 will be to involve more institutional investors and to increase the share of international investors in Italian VC-led rounds. There is still a long way to go, but the positive signs of the last year tell us that the path we have taken is undoubtedly the right one,’ adds Francesco Cerruti .

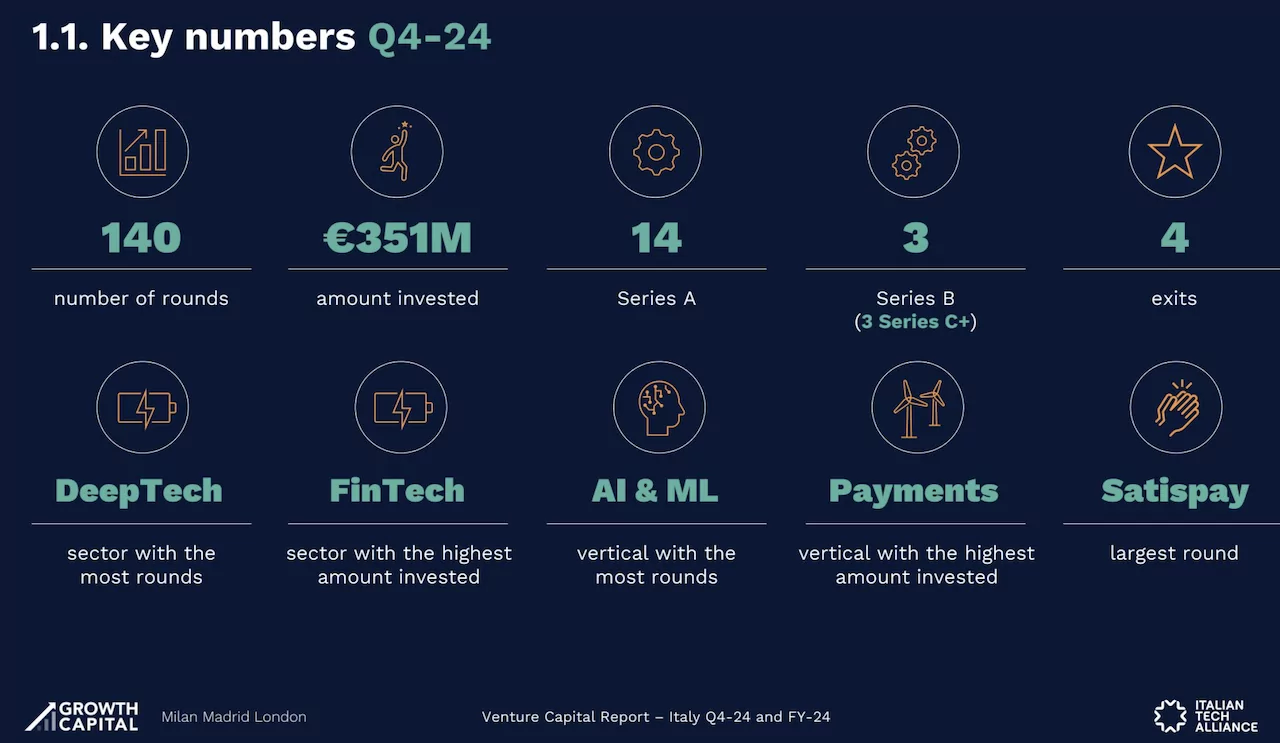

The observatory also released figures for the fourth quarter of 2024, which saw investments amounting to EUR 351 million in 140 rounds.

ALL RIGHTS RESERVED ©