Table of contents

“The numbers of this last quarter and in general those of the first nine months of 2024 are comforting, because they testify to a recovery of investments and a substantial resilience of VC in Italy. – says Francesco Cerruti, General Manager of Italian Tech Alliance, commenting on the start-up investment figures for the third quarter of the year as revealed by the usual report produced by Growth Capital – Nevertheless, much is still needed to foster the growth of the number of rounds, attract a broader range of investors, and reduce the gap with other European countries. In order to do so, it is necessary to modernise the regulations governing the sector to attract investment and support innovation entrepreneurs. For this reason, we are working to ensure that the innovation-related regulatory interventions contained in the Ddl Concorrenza, which currently fall short of the needs and expectations of the Italian innovation ecosystem, can be strengthened in the coming months by further measures’.

With regard to the package of regulations known as the Startup Act, we should also bear in mind the news of the last few days that the VI Finance Commission in the Chamber of Deputies has given the Honourable Giulio Centemero the mandate to bring the PdL Startup, which, as per the procedure, will become law after passing through the Chamber.

The data

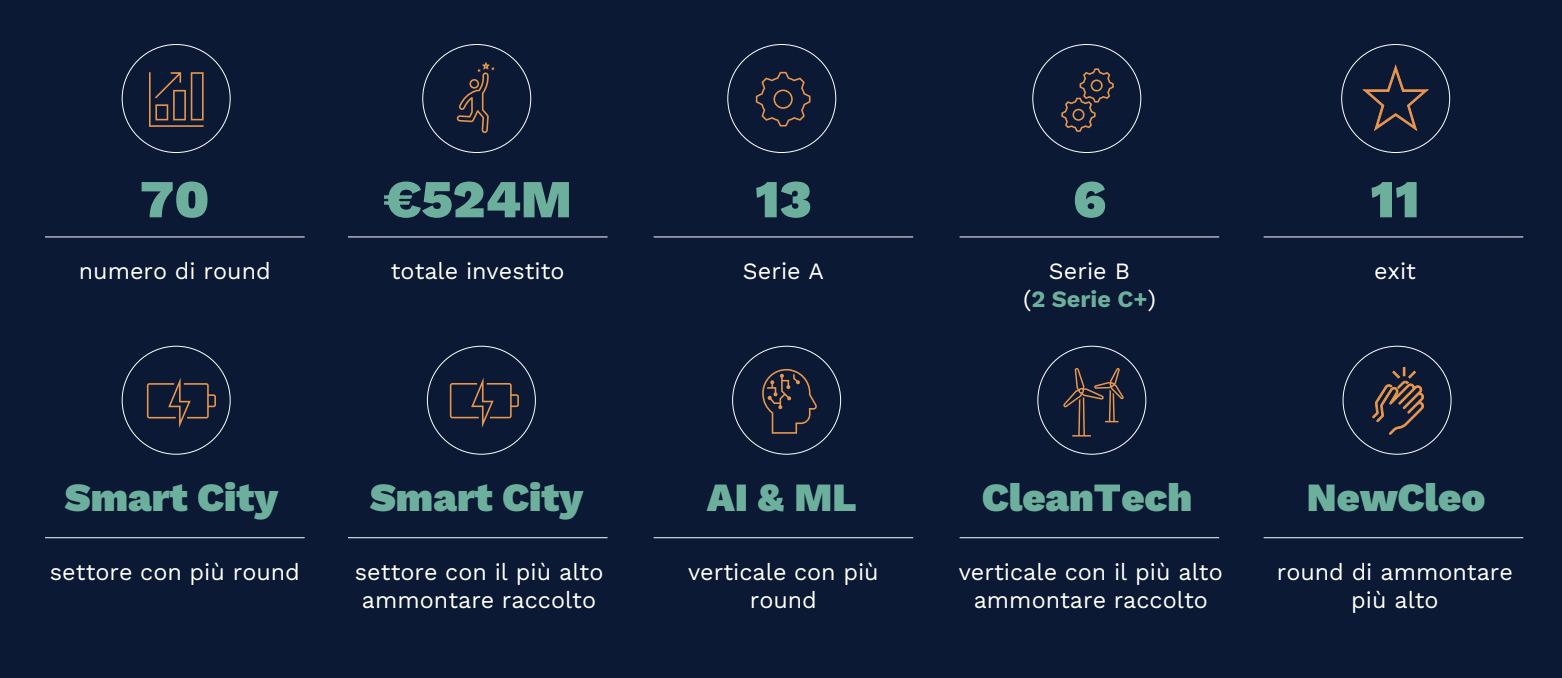

According to Growth capital’s report, Italian venture capital investments exceeded EUR 524m in Q3 2024, with 70 investment rounds (of which 13 series A and 6 series B) and 11 exits all registered through M&A. Compared to previous quarters (69 in Q2, 70 in Q3), the amount more than doubled from 226 million in Q2 to 524 million in Q3. Looking ahead to 2024 as a whole, 247 rounds were closed in the first nine months (of which 37 Series A and 10 Series B) for an invested amount of EUR 1.195 billion – a third of which can be attributed to three mega rounds -, thus surpassing the total investments for the whole of 2023 and thus resulting in the best quarter in the last two years. There were 31 exits, while software was the sector with the largest number of rounds and smart cities the one with the highest number of rounds. According to Fabio Mondini de Focatiis, founding partner of Growth Capital, “in terms of invested capital, Italy will be one of the ecosystems with the highest growth compared to the previous year” and in fact “is catching up with the other EU countries”. “To date, Italy has halved its difference with the other countries.”

In Q3 2024, pre-seed and seed are the most frequent type of rounds (63% of the total), although lower than in the first half of the year (71%), while 45% of the total funding came from Series B and higher rounds.

Looking at the individual sectors, smart city (EUR 207 million) ranks first in terms of amount invested, followed by life science (EUR 69 million) and deeptech (EUR 66 million). By number of rounds, smart city has 13, software 12 and fintech 8. In the first nine months of 2024, we see €341m invested in smart city, followed by life science (€236m) and software (€228m); software has the most rounds (37), followed by smart city (34) and life science (32).

Leading the top 5 deals of the quarter is NewCleo (EUR 135m, Series A), followed by D-Orbit (Series C, EUR 50m) and Genespire (Series B, EUR 46.6m). Then Limolane and Bizaway, which both raised EUR 35m each in a Series B round.

With zero IPOs and 11 exits, according to Fabio Mondini de Focatiis, even ‘fewer IPOs and exits are expected in the near future‘. This is because in recent years most Italian start-ups have not wanted to make rounds. Now, however, capital is beginning to be scarce, and for Mondini de Focatiis a useful tool could be that of buy and build, derived from private equity: “we are helping many start-ups to acquire other start-ups that today ‘are at the brink’ precisely because they did not want to raise”.

CEO Agostino Scornajenchi spoke at the event, which was also organised in collaboration with CDP Venture Capital: ‘the year was very positive because we made it clear that venture capital in Italy is to all intents and purposes a fully-fledged part of the institutional entrepreneurial chain. We are not something different from companies, we are the factory of companies‘. Scornajenchi then made a very interesting parallelism alluding to the automotive market – today the Italian one is in the midst of a crisis -: ‘on the other side of the ocean 30 years ago they had motor companies, large oil companies, and today they have a digital ecosystem: companies that are not new, because Apple is almost 50 years old, but in the meantime that those same crises in industrial sectors were biting us – look at the fact that the automotive crisis in the US was worse than ours – new sectors were growing, supported by venture capital.

On the other hand, according to Giuseppe Donvito, president of Italian Tech Alliance and partner at P101, even if the third quarter numbers are positive, the glass is still half-empty: on the one hand, ‘there is still a minimum of asymmetry because in the last five years the pre-seed has collapsed’ and on the other hand, this has meant that in this range ‘the deal-flow is not exciting, because in VC there are cyclical effects’ and ‘if the initial base is missing, the pyramid does not hold’. If we then look at who innovates, while in the US it is the universities, in Italy it is mostly the corporations, and “the spin-off world in Italy is still struggling”.

AI in Italy

In the first half of 2024, start-ups using artificial intelligence raised EUR 57 million, or 8% of the total amount invested. This is lower than in the EU (22%) and the US (41%).

According to Scornajenchi, ‘the fund in IA was legally launched this summer and the total intervention is one billion euro. The amount invested to date is over 100 million, so we are there’. With regard to our type of AI, Scornajenchi emphasises how we could be competitive: ‘there is a sector, where in my opinion a country like ours can truly express a distinctive competence, which are the vertical industrial applications enabled by artificial intelligence: to what extent does artificial intelligence make a press work better, to what extent does artificial intelligence help, speed up the search for a drug. We have mechatronics, precision mechanics, industrial packaging, all verticals that we have developed and exported to the rest of the world. The Americans are putting in money en masse, but this type of technology has always come to us in recent decades’. In conclusion, he pointed out the other side of the AI coin, which is often still considered taboo: the green issue, which, in the field of mechatronics, would cost less. In fact, according to the CEO of CDP VC, ‘in the Milan area alone, 6,000 megawatts per day must be available, and for that we need 6 nuclear plants of 1,000 megawatts each, and there is not that stuff in Italy today, it has to be imported’. So ‘we need major powers. As you have seen, large industrial groups in the United States, but also in Italy, are beginning to address the issue of how to bring together artificial intelligence and the need for data centre consumption with energy production. This is another challenge: to what extent consumption can be reduced by intelligent use of this technology’.

ALL RIGHTS RESERVED ©